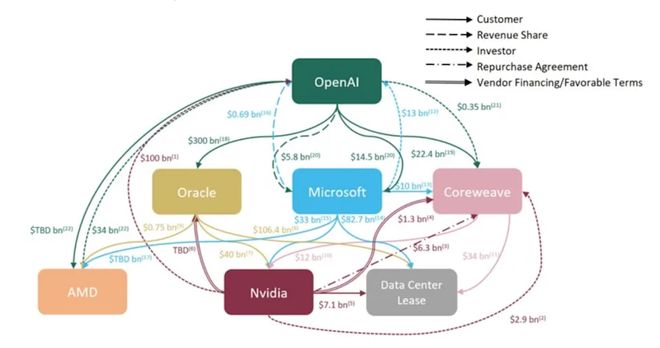

Companies at the center of the artificial intelligence (AI) boom are investing billions in each other, but Wall Street analysts are warning that this growing "entanglement" is increasing the risk of an AI bubble. At the end of September, Nvidia said it would invest up to $100 billion in ChatGPT maker OpenAI and use Nvidia's chips to train and run its next-generation model.

And it's just one of a string of deals at major tech companies that have become public over the past few months. Nvidia also struck a $6.3 billion deal with AI data center company CoreWeave, a customer of Nvidia in which Nvidia holds a 7% stake. Nvidia also invested $2 billion in its customer xAI. In addition, OpenAI has reached agreements with Oracle, CoreWeave and chipmaker AMD.

One loses and all loses

Wall Street analysts said the agreements underscore a growing trend: Artificial intelligence infrastructure providers, led by Nvidia, are investing in their customers, who then turn to buy more infrastructure providers. And infrastructure customers like OpenAI are investing in its suppliers.

Wall Street analysts say there are two main concerns about this "cyclical dynamic" amid the recent AI investment boom. First, the nature of the deal may make it appear that the need for AI is greater than it actually is. At the same time, it's also driving closer links between Big Tech's valuations — especially given their respective stocks soared on news of such deals, intertwining their fortunes.

Therefore, a hit to any one company would spell bad news for the entire ecosystem.

Kim Forrest, a technology analyst and chief investment officer at Bokeh Capital Partners, said: "The latest developments are very disturbing. (Artificial intelligence infrastructure) vendors are making a lot of money, so they are just stuffing money back to customers, and it may be spent in the wrong place."

Cornell University professor Karan Girotra said instances of suppliers and customers supporting each other financially reduce the "resilience" of the entire system: "If something goes wrong, the impact spreads to the entire system, rather than being isolated."

Jim Chanos, the legendary short seller best known for predicting the collapse of Enron during the dot-com bust, also weighed in last week, posting on

Learn from history

Why might this type of circular investment be risky? Experts point to the clearest example of this occurring during the dot-com bubble of the late 1990s and early 2000s. As the Internet boomed, Internet service providers (ISPs) rushed into the market of providing networks and access to the Internet, but soon found themselves strapped for cash.

It’s similar to the recent spate of AI deals, when vendors of equipment — including routers, switches, fiber-optic cables and other hardware that will bring consumer internet to the mass market — are investing in internet service providers (their customers) through loans and equity stakes. ISPs can then use these loans and equity financing to purchase routers or cables from equipment companies—a deal known as "vendor financing."

On the surface, everything is booming and deals are huge. Between 1999 and 2001, equipment vendors such as Cisco Systems, Nortel Networks and Lucent provided billions of dollars in loans to Internet providers and telecom operators. But when capital dried up, dozens of ISPs went bankrupt.

As the industry spiraled downward and the dot-com bubble burst, vendors' misinvestments in their customers exacerbated the impact of its collapse. Data show that from March 2000 to the end of 2002, the Nasdaq Composite Index, which is dominated by technology stocks, fell by more than 70%, with losses equivalent to more than 3 trillion US dollars.

Too much reliance on OpenAI

Wall Street analysts are particularly concerned that the “tangle” of investments in artificial intelligence is making the system too dependent on OpenAI’s success. The ChatGPT maker has yet to turn a profit, and analysts are worried about what will happen if the company's revenue doesn't meet expectations.

Bernstein analyst Stacy Rasgon wrote in an Oct. 6 report:"[OpenAI CEO Sam Altman] has the ability to collapse the global economy for 10 years, or he has the ability to take us to the Promised Land, and we don't know which scenario is going to happen yet."

DA Davidson analyst Gil Luria said some recent transactions are particularly concerning because artificial intelligence companies such as OpenAI and CoreWeave have taken on more debt or announced intentions to do so while accepting investment from Nvidia.

"They use these funds to borrow, and leverage is really unhealthy behavior," he said.

Cory Johnson, chief market strategist at Epistrophy Capital Research, also said that such an arrangement is a sign of an unhealthy ecosystem: "If your customer has to borrow money to buy your product, then your customer is not a good customer."