Apple is about to launch its first foldable screen iPhone "iPhone Fold" at the end of 2026. This new product not only marks Apple's official entry into the folding smartphone field, but is also regarded as a key force in promoting the recovery of global folding mobile phone screen shipments in 2026. The latest forecast from market research firm Counterpoint Research shows that the folding screen panel used in the iPhone Fold will account for about 29% of global folding smartphone display orders in 2026, second only to Samsung, which is expected to remain in the lead, and far ahead of major competitors such as Huawei.

According to a Counterpoint Research report, Samsung is expected to continue to top the list of foldable phone screen orders in 2026 with a share of about 31%, followed by Apple iPhone Fold with a share of 29%, and Huawei is expected to gain a market share of about 24%. The industry believes that as Apple’s first folding model joins the fray, the product structure and price system of the folding screen market will undergo significant changes. The high-end full-size “book-style” folding form is replacing the “clamshell” folding machine with a relatively low price as its selling point and becoming the mainstream. The report pointed out that Apple's entry will push the overall average selling price higher, but "the growth of the foldable inside-out form does not entirely depend on Apple." High-end product lines from manufacturers such as Samsung and Huawei are also driving this trend.

In terms of more cutting-edge multi-folding forms, such as the Huawei Mate XT series and the rumored Samsung Galaxy Z TriFold and other three-folding devices, it is still difficult to move towards the real mass production and popularization stage in the short term. The report analyzes that the three-fold design still faces major challenges in yield control and process complexity, and these factors will continue to limit the widespread implementation of this form in the short term. In contrast, bi-folding book-style products have gradually matured through multiple generations of iterations, and their balance in size, durability and user experience are more suitable to become mainstream high-end folding solutions.

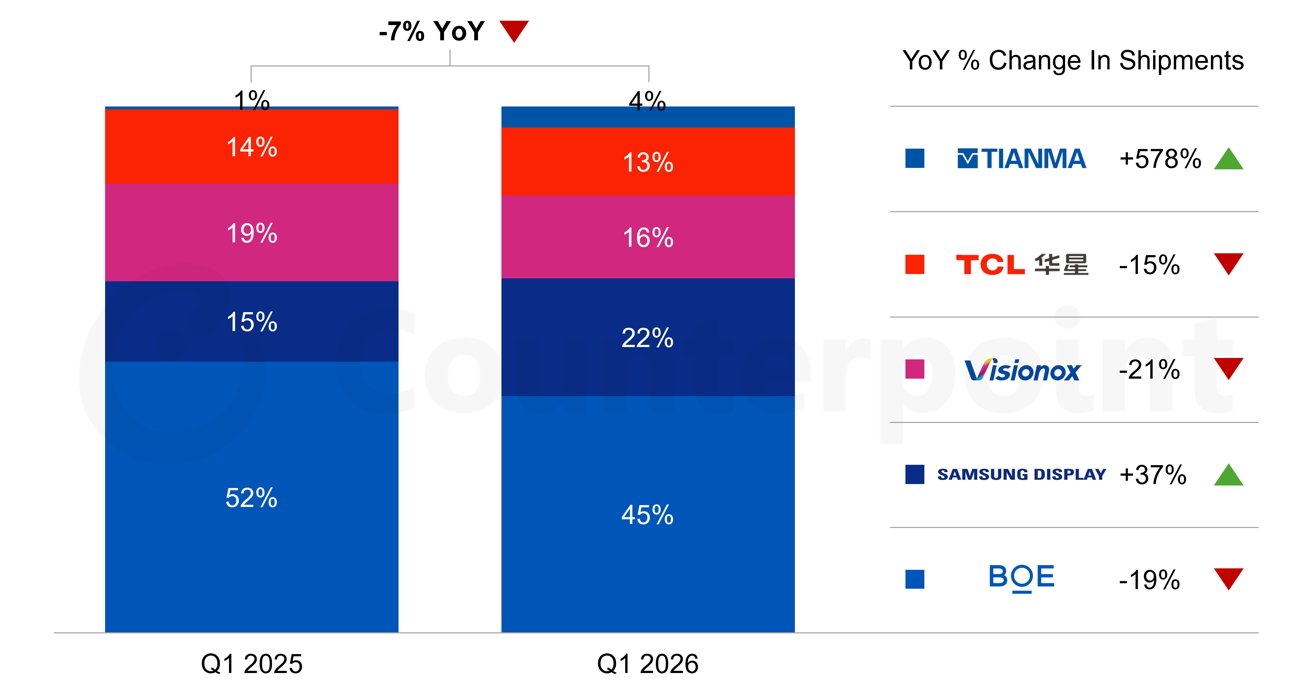

At the supply chain level, news and rumors from multiple channels all point to the same conclusion: the supplier of the OLED folding panel used in the iPhone Fold will be Samsung Display. Research data points out that Samsung Display has accounted for 22% of folding smartphone screen shipments in the first quarter of 2026, a significant increase from 15% in the first quarter of 2025. However, overall, the folding screen panel market is still dominated by Chinese panel manufacturer BOE, whose share in the first quarter of 2026 is approximately 45%, although it has declined from the previous 52% share.

At the same time, the unsatisfactory cooperation between Apple and BOE on high-end iPhone panels has also affected the supply judgment of future folding products. There are rumors that Apple has decided not to use BOE's OLED panels on the upcoming iPhone 18 Pro in April 2026. This is also regarded by the industry as a signal that BOE will find it difficult to enter the iPhone Fold project in the short term. Based on current information, Apple’s folding screen supply chain will rely more on Samsung Display’s mature folding OLED technology to ensure the display quality and reliability of the first folding iPhone.

Looking at the overall market size, global foldable smartphone screen shipments are expected to reach approximately 27.5 million units in 2026, an increase of approximately 24% compared to 2025. This increase is particularly noticeable in the context of the current slowdown in the overall smartphone market. Analysts generally believe that iPhone Fold panel orders from Apple will become one of the important factors driving this growth. Before Apple officially entered the market, the folding screen market was driven more by the Android camp. Now with the arrival of iPhone Fold, the folding form is expected to move from niche to high-end mainstream and become an important branch of flagship models.