Morgan Stanley's latest report pointed out that as the construction of artificial intelligence infrastructure accelerates, the demand for electricity in U.S. data centers is rising sharply. It is expected that there will be a power gap of up to 44 gigawatts by 2028, which is equivalent to the power generation of 44 nuclear power plants. The report believes that without improving power supply capabilities through natural gas turbines, fuel cells, or Bitcoin mine transformation, the U.S. energy system may not be able to support the expansion of the AI industry.

Morgan Stanley recently released a latest report stating that the construction of artificial intelligence (AI) infrastructure in the United States is driving domestic power demand to enter a new stage, and power supply capacity may become a key limiting factor in the expansion of the AI industry.

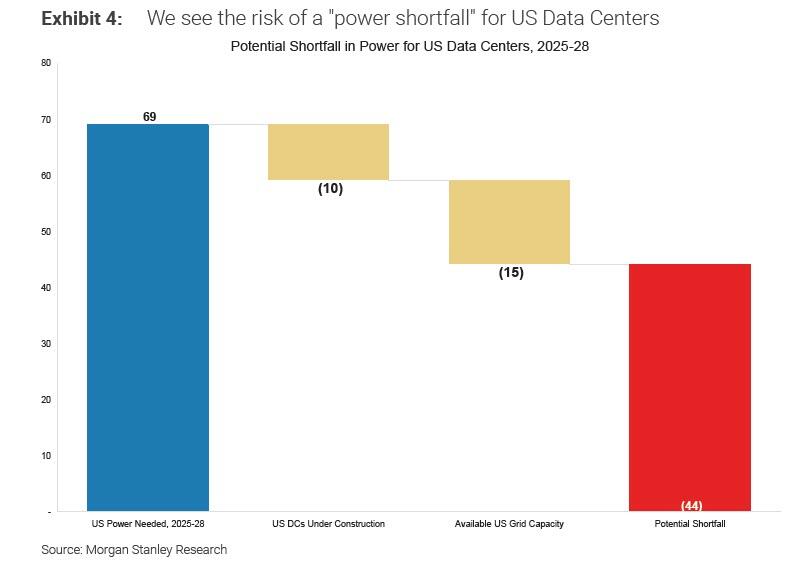

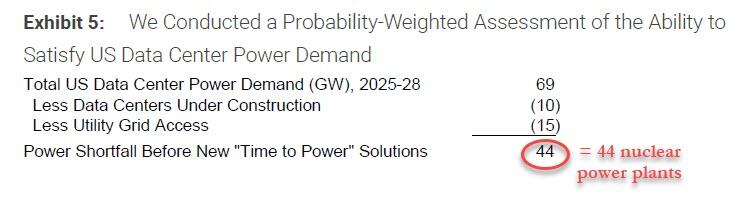

The bank's strategist Stephen Byrd pointed out in a research report titled "Powering AI: Bitcoin Conversion, Business Models, a US Power Shortage and the Big Picture", total power demand for U.S. data centers is expected to reach approximately 69 gigawatts (GW) by 2028. Among them, about 10 GW comes from data centers under construction, and another 15 GW can be connected through the existing power grid, but there is still a power gap of about 44 GW.

This latest figure is a further upgrade from Morgan Stanley’s December forecast of a 36 GW shortfall. The report pointed out that if converted according to the power generated by nuclear power plants, 44 gigawatts is equivalent to the size of approximately 44 nuclear power plants.

The report mentioned that the Loan Programs Office under the U.S. Department of Energy recently stated that it is ready to provide hundreds of billions of dollars in financing to nuclear power projects to promote the construction of clean energy capacity and relieve potential power supply pressure.

Morgan Stanley believes that power supply shortages may affect the implementation and pace of AI-related investments. According to estimates, the construction cost of each additional 1 GW of data center capacity is approximately US$50 billion to US$60 billion. Insufficient power access capabilities may lead to a longer AI infrastructure construction cycle.

Morgan Stanley emphasized that there are currently no new nuclear power reactors under construction in the United States. Considering that the nuclear power construction cycle usually takes more than ten years, if the United States does not improve its power supply capacity in the short term through natural gas, fuel cells, and inventory facility renovation, it may not be able to support the rapid expansion of AI infrastructure.

Time to Power Solution

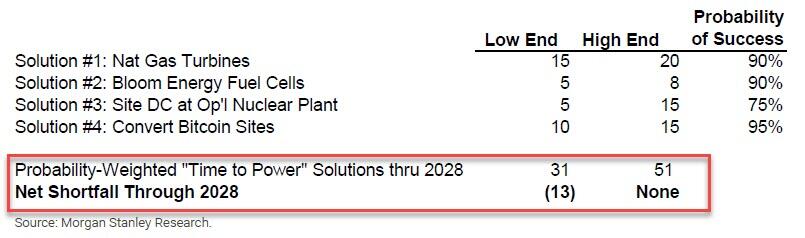

To solve this problem, Morgan Stanley has proposed a number of "Time to Power" solutions, which are alternative measures that do not rely on the traditional grid connection process and can provide power faster. Assuming that all these plans are implemented, the U.S. power gap can be reduced to about 20% by 2028, equivalent to 13 gigawatts, which is still about the power generation of 13 nuclear power plants.

The report lists several potential options:

Natural gas turbine projects can add approximately 15 to 20 gigawatts of electricity;

Fuel cell company Bloom Energy can contribute 5 to 8 GW (if its annual production capacity is increased to 3 GW, potential supply can be further expanded);

Transactions to provide direct power to data centers from existing nuclear power plants could bring in approximately 5 to 15 GW (excluding indirect use of new natural gas generation to offset nuclear power use, which is already included in the 20 GW natural gas turbine projects mentioned above);

In addition, Morgan Stanley estimates that existing Bitcoin mining farms already have large (over 100 MW) sites with complete access protocols, totaling about 20 GW of potential capacity, which can be converted into 10 to 15 GW of actual supply.

Among these plans, Morgan Stanley believes that the plan to transform Bitcoin mines into AI data centers has obvious advantages in terms of execution speed and risk control, and may gain higher market recognition in the future. The report also pointed out that Bloom Energy's fuel cell system is also a reliable "quick power supply" approach and is expected to drive rapid growth in the company's shipments.

In addition to fuel cell and Bitcoin mining farm conversions, Morgan Stanley expects a diversified "Time to Power" transaction model, involving independent power producers, turbine manufacturers and energy companies.

Bitcoin mine transformation data center attracts attention

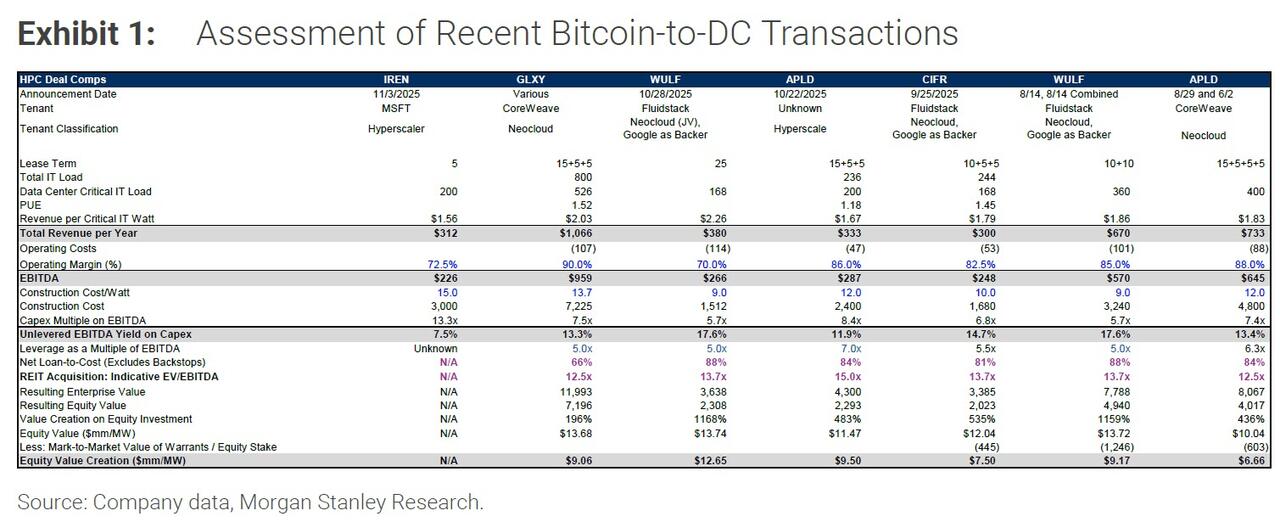

Against the background of the rapid growth in demand for AI computing power, Morgan Stanley is particularly concerned about the transformation trend of Bitcoin mines into high-performance computing (HPC) data centers. The report points out that there are currently two main business models in the industry: one is the "New Neocloud" model, represented by IREN, in which mining companies purchase GPUs or TPUs, build their own data centers, and then lease computing power facilities to ultra-large-scale cloud service providers or enterprise customers for a short period of time. For example, IREN signed a five-year lease with Microsoft.

The second is the "REIT Endgame" model, in which mining companies are responsible for building the "charged shell" (that is, infrastructure other than chips and servers) and signing long-term leases with cloud computing companies. For example, APLD signed a 15-year lease with an undisclosed cloud service provider.

Morgan Stanley believes that both models have considerable value creation potential and demonstrate the transformation path of traditional cryptocurrency infrastructure into the field of AI computing.

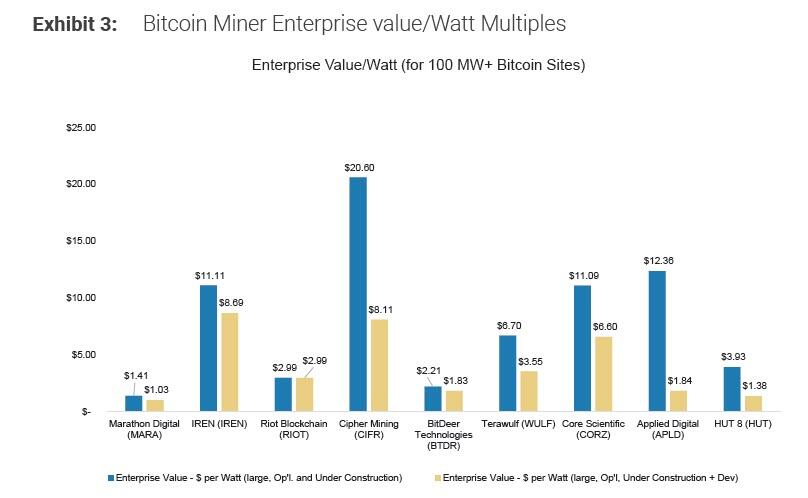

At the end of the report, the report also provides valuation reference data for Bitcoin mining farm transformation data centers, showing that currently large mining farms with stable power grid access and installed capacity of more than 100 megawatts have large differences in enterprise value/watt (EV/W) multiples. Morgan Stanley noted that the lower the valuation multiple, the more attractive the potential conversion opportunity is.