According to news on July 3, Tesla’s second-quarter deliveries significantly exceeded market expectations, but investors did not regard this delivery data as unconditionally positive. The company's shares closed down 7.5% at $393.45, the largest one-day drop in about a year.

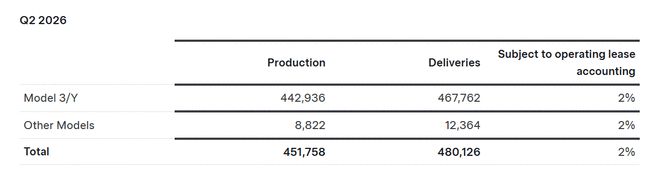

On Thursday, Tesla released production, delivery and energy storage deployment data for the second quarter of 2026: 451,758 vehicles were produced in the quarter, 480,126 vehicles were delivered, and energy storage product deployment was 13.5GWh. For comparison, Tesla's average market forecast announced on June 26 was 406,024 units; CNBC cited StreetAccount's expectation of about 406,600 units.

Calculated by these two calibers, Tesla’s actual delivery volume was approximately 74,000 vehicles higher than expected. This is an extremely rare surprise.

Taking it apart, Model 3 and Model Y are still the absolute mainstays. In the second quarter, Tesla produced 442,936 Model 3/Y units and delivered 467,762 units; it produced 8,822 units of other models and delivered 12,364 units. Deliveries were about 28,000 vehicles higher than production, indicating that Tesla digested some of its previously accumulated inventory during the quarter.

This data gives Tesla a long-lost sales rebound narrative. According to Electrek's calculations based on Tesla's historical data, the delivery volume of 480,126 vehicles increased by approximately 25% from 384,122 vehicles in the second quarter of 2025, and increased by approximately 34% from 358,023 vehicles in the first quarter of 2026. This is also the strongest second-quarter delivery performance in Tesla’s history, exceeding the 466,140 vehicles in the second quarter of 2023.

But the stock price reaction was uncooperative. The market's attitude is straightforward: This delivery data is indeed impressive, but it is not enough to further increase Tesla's price.

The reason is that there are still several question marks left over this time beyond expectations.

First, whether the rebound in sales is sustainable.CNBC mentioned in the report that Tesla has experienced a decline in annual car sales in the past two years, with pressure coming from multiple directions: consumer resentment caused by Musk's political remarks, changes in the U.S. federal electric vehicle tax credit policy, and intensifying competition from Chinese, Korean and European car companies. In order to boost sales, Tesla has launched lower-priced versions of Model 3 and Model Y, and is promoting FSD supervision versions in some European markets.

Second, delivery is higher than production, which is not completely equivalent to a full outbreak of new demand.About 28,000 more vehicles were delivered than produced, which means inventory digestion participated in this quarter's performance. The decline in inventory is a good thing in itself, but whether it can continue to deliver a figure close to 480,000 vehicles next season depends on whether real orders can keep up.

Third, Tesla’s valuation has been betting beyond electric vehicles.Energy storage deployment this quarter was 13.5GWh, higher than the 9.6GWh in the same period last year, but lower than the market expectation of 13.8GWh announced by Tesla. The energy storage business is still growing, but it just didn't beat expectations as significantly this quarter as car deliveries did.

Tesla itself also reminded in the announcement that delivery volume and energy storage deployment are only two indicators of the company's financial performance and cannot be used as a complete substitute for quarterly financial results. Key data such as net profit, cash flow, average selling price, cost structure, and foreign exchange impact in the second quarter will not be revealed until the official financial report is released after the market closes on July 22.

Tesla has delivered a strong sales quarter, but investors are still waiting for several other answers: whether real orders can keep up after inventory is digested, whether the energy storage business can continue to accelerate, and whether autonomous driving, Robotaxi and robotics businesses can support current valuations.

The next test point is the earnings call on July 22. The delivery data has already won the game, and the question to be answered by the financial results is: How much money did Tesla make after these cars were sold.