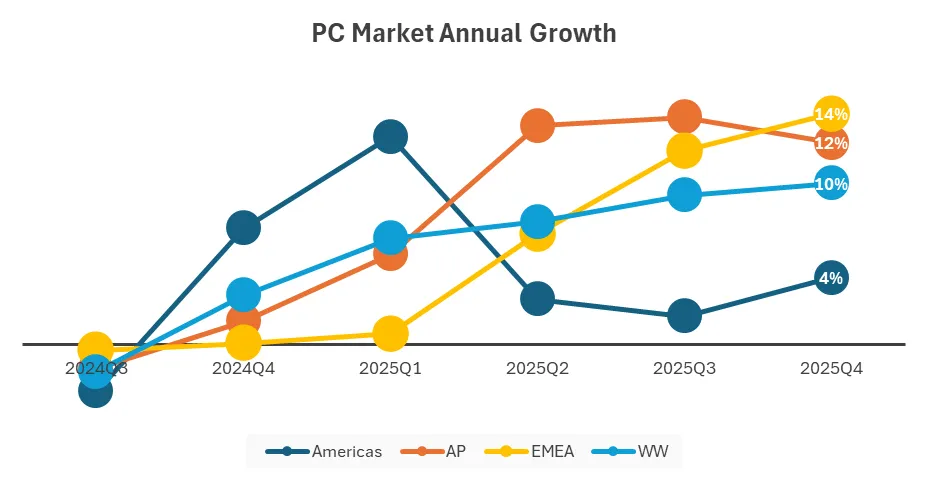

In the fourth quarter of 2025, global PC shipments unexpectedly achieved nearly 10% year-on-year growth amid tight memory supply, with total shipments reaching 76.4 million units, exceeding industry expectations. Market research firm IDC pointed out that this growth not only benefits from the traditional peak season at the end of the year, but is also closely related to manufacturers and channels preparing in advance to cope with potential tariffs and global memory shortages.

Microsoft is about to end its support for Windows 10, which is one of the important drivers of this round of PC update waves. A large number of corporate and individual users have replaced or upgraded their equipment in advance, boosting the shipment of complete machines. At the same time, PC manufacturers are actively "rushing" at the end of 2025 and accelerating the lock-in of inventory to keep overall costs as low as possible before the price upward cycle expected in 2026. IDC bluntly stated in the report that it is "the emergence of a new round of memory shortages that has caused buyers and brands to step up their efforts to lock in inventory at the end of 2025 to cope with the expected price increases in 2026."

The current surge in memory and NAND/SSD prices is due to the substantial expansion of demand for AI data centers, which has severely squeezed memory chip production capacity. Major PC manufacturers such as Lenovo and HP have been actively hoarding memory in the past few months, but IDC predicts that these inventories are likely to be exhausted in the next few months, and then the pressure to increase machine prices and even passively lower product configurations will be fully apparent.

Jean Philippe Bouchard, vice president of research at IDC, warned that in addition to the overall price increases that some manufacturers have publicly announced, the market may also see average memory specifications being actively lowered to extend the service life of existing inventory. He believes that this will make the PC market in 2026 highly uncertain and "extremely volatile", with prices and configurations subject to frequent adjustments.

In terms of price strategy, IDC predicts that the average selling price of PCs will rise overall in 2026, and manufacturers will prioritize resources on mid- to high-end and high-end models to hedge against rising memory costs with higher unit prices. This trend, coupled with factors such as AI acceleration and computing power competition, means that the entire PC industry will be in an AI-driven "storm" in 2026, and channels, brands and consumers will all need to face the continuous reconstruction of prices and configurations.

In such an environment, IDC focuses on end-user consumption decisions and believes that if there is a clear purchase plan, the sooner you enter the market in 2026, the more likely you are to avoid subsequent price increases and potential allocation shrinkage risks. For ordinary consumers and enterprise users, completing machine replacement or capacity expansion in advance is expected to lock in relatively better prices and product parameters to a certain extent, and obtain a "stability window" before the upcoming violent fluctuations.