According to Omdia's latest research, affected by the rapid rise in DRAM and NAND prices, smartphones priced under $400 globally are facing unprecedented cost pressure. In 2026, smartphone shipments in this price range are expected to decline by more than 22% year-on-year.

This analysis is the first of a two-part series, focusing on how rising memory prices will reshape the cost structure of smartphones, focusing on mid- to low-end models and accelerating the shrinkage of the smartphone market below US$400. The second article will further explore how cost pressure exacerbates the "memory polarization" of the smartphone market: manufacturers reduce or freeze memory capacity on mid- and low-end products, while continuing to improve configurations on high-end products.

Omdia's latest research shows that DRAM and NAND prices have risen sharply in the past few quarters, and are expected to continue to rise in the future. Memory costs have become a heavy burden on low- and mid-range smartphones and are driving the sub-$400 smartphone market to see an annual decline of more than 22% through 2026.

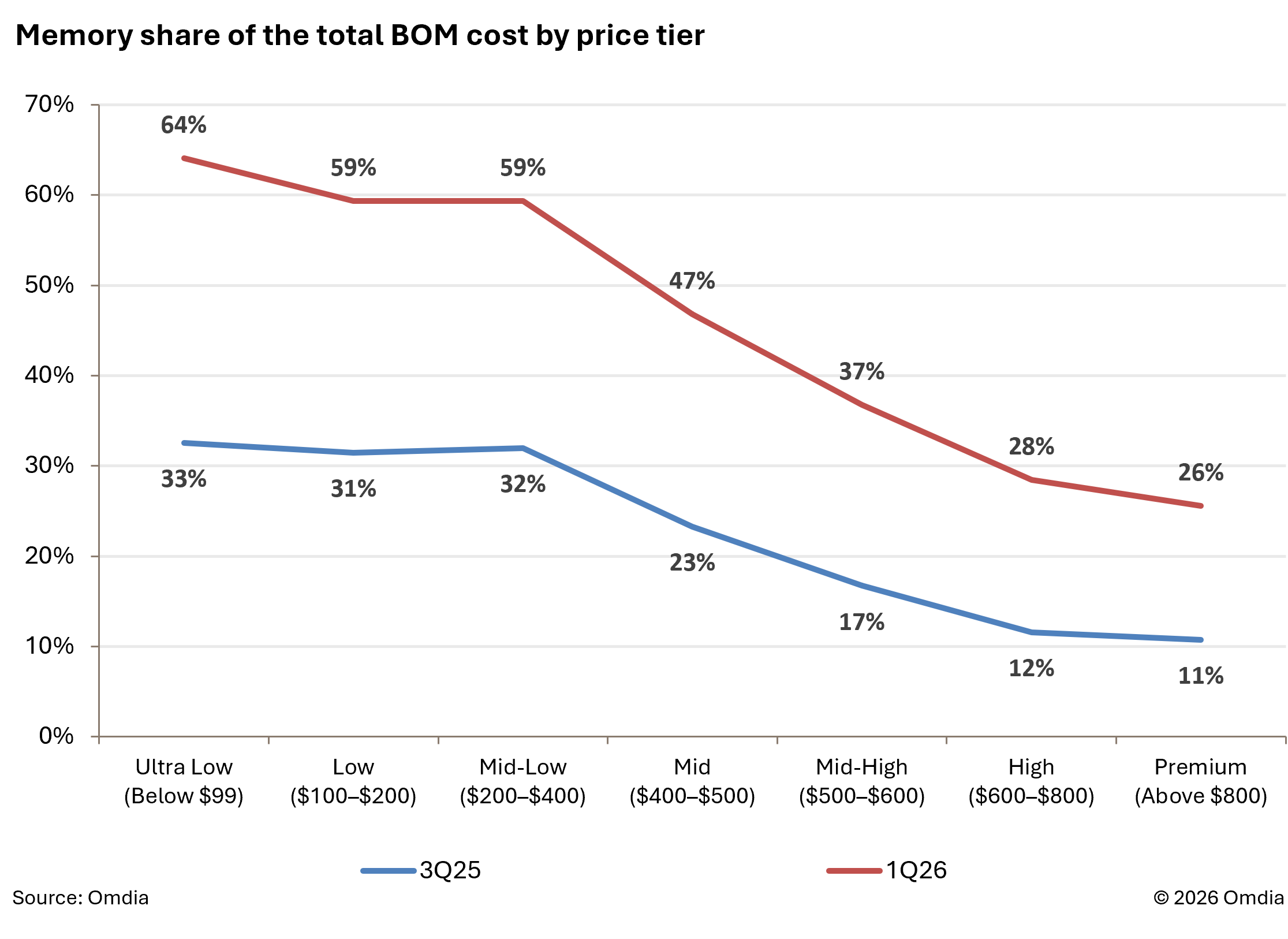

Compared with the third quarter of 2025, the material cost (BOM) structure of smartphones in the first quarter of 2026 has changed significantly. In models priced below $400, the memory cost ratio has almost doubled; in products priced above $400, the memory cost ratio has also more than doubled. Omdia's "Quarterly Smartphone Technology Trends - High-End Edition for the First Quarter of 2026" report points out that in the first quarter of 2026, the cost of memory in smartphones under US$400 has accounted for nearly 60% of the BOM cost of the entire machine. Among products priced below $99, this proportion is more than 64%.

In order to alleviate the pressure caused by soaring memory costs, smartphone manufacturers are trying to reduce costs on other components, including display panels, sensors and radio frequency (RF) modules, which are in relatively abundant supply. However, low-end smartphones are inherently designed on an extremely tight cost structure, making it extremely difficult to offset higher memory costs by cutting other components. Zaker Li, chief analyst of Omdia's consumer electronics team, pointed out that as memory prices continue to rise in the next few quarters, the cost pressure on low-end smartphones will only worsen.

In the current environment, many smartphone manufacturers including Transsion, OPPO, vivo, Honor and Xiaomi have been forced to significantly increase the retail prices of their products just to maintain slim profit margins. But for low-end consumer groups who are highly price-sensitive, rising retail prices are bound to significantly suppress demand. Judging from the memory price trend in the next few quarters, many low-end products have actually gradually entered the "unprofitable" range. As terminal selling prices continue to rise, the risk of weak demand has increased significantly. Against this background, manufacturers are actively and gradually withdrawing from the low-end market this year.

Omdia's latest forecast in May this year shows that the overall global smartphone market shipments will decline by approximately 12% year-on-year in 2026. This decline is mainly driven by a significant decline in product shipments in the price segment of $400 and below, with shipments of models in this price segment expected to decrease by more than 22% this year. In contrast, smartphones priced above $400 are expected to remain resilient in 2026, with shipments expected to achieve 5.7% year-over-year growth.

There are three key factors behind the relatively solid performance of the high-price segment. First of all, smartphone manufacturers are accelerating the shift of resources and strategies to mid- to high-end product lines. Secondly, terminal retail prices continue to rise, pushing more models into the price range above US$400, thereby expanding the market share in this price range. Finally, the overall low price sensitivity of high-end consumers helps support stable demand for such products.

Among mid-to-high-end and flagship models, manufacturers have more room to reduce configurations to partially offset memory cost pressures. As the price level increases, the proportion of memory cost in models priced above US$400 will decrease rapidly. For products above US$600, components such as high-specification application processors (SoCs), displays, and camera modules account for a significant increase in the BOM of the entire machine. Manufacturers can adjust around these specifications to alleviate cost pressures.

In terms of display, some Chinese smartphone manufacturers have begun to return to LTPS OLED panels on some high-end models, replacing the LTPO display technology used in previous upgrades, while mainly retaining LTPO on more top-end flagship models. This strategy is expected to save about $3 to $5 per phone. In terms of camera modules, manufacturers can flexibly configure according to different product positioning, such as using smaller image sensors or reducing the number of cameras, thereby controlling costs.

In terms of application processors, SoC still accounts for the largest cost component for smartphones priced above US$600. Manufacturers can reduce costs by about 30% to 40% by slowing down the pace of platform iteration and using more previous-generation processor platforms. As memory costs continue to reshape the economic structure of smartphones, manufacturers must make a more careful balance between "affordability", "profitability" and "product competitiveness".