In the third quarter of 2025, the global smartphone market will see warmth again. Omdia data shows that global shipments increased by 3% year-on-year in the third quarter. The rebound in this quarter was due to strong replacement demand and the fact that many manufacturers stocked channels in advance before the busy fourth quarter of 2025.

Among them, Samsung and Apple rank top two in the world in terms of market share, but Apple’s new phone portfolio is uneven.

Data from multiple institutions show that despite the outstanding performance of the iPhone 17 series, the shipments of the new product line iPhone Air are limited. Tianfeng International Securities analyst Ming-Chi Kuo said that iPhone Air demand is lower than expected, and supply chain production capacity will generally be reduced by more than 80% by Q1 2026. Some components with long shipping lead times are expected to cease production before the end of 2025.

Looking at the domestic market, Omdia data shows that in the third quarter, the smartphone market in mainland China fell by 3% year-on-year. However, structural adjustment has accelerated and the competitive landscape has been reshaped. Vivo has returned to the first place, Huawei has climbed to second place, and the industry is moving from "quantitative competition" to "qualitative upgrade."

Overall, Liu Yixuan, head of mobile phone industry research at Omdia, told a reporter from the 21st Century Business Herald: "We estimate that from 2025 to 2029, the global smartphone market will grow by 54 million units in shipments, of which nearly 70% will come from growth in emerging markets."

At the same time, AI intelligence and form innovation have become the growth engines of the new cycle. From the recovery of replacement demand to the construction of ecological barriers, from global expansion to high-end breakthrough, the smartphone industry is in a new transformation period.

Replacement demand recovers and global competition escalates

From the perspective of the global market, the growth momentum of the mobile phone industry in the third quarter comes from two directions. One is that with the arrival of the replacement cycle, global replacement demand is gradually released. Second, innovations in hardware and AI experience by major manufacturers have reactivated consumer willingness.

The ranking is still concentrated on the top companies. Omdia data shows that among the top five manufacturers in the world, Samsung ranks first for the third consecutive quarter with a market share of 19%, benefiting from the hot sales of the Galaxy A series and the upgrade of the seventh-generation foldable machine.

Apple's performance was particularly strong, with iPhone shipments increasing 4% year-on-year, setting a record for the third quarter in history. Advance demand for the iPhone 17 series pushed its market share to 18%, becoming an important driving force for the rebound this quarter.

In addition, Xiaomi performed stably this quarter, with a market share of 14%, while Transsion and vivo each accounted for 9%, jointly ranking among the top five manufacturers this quarter.

Omdia Research Manager Zhou Lexuan pointed out: "Consumers' demand for smartphone upgrades and replacements is recovering, which has pushed the market to regain growth momentum after experiencing fluctuations at the beginning of the year. Judging from the performance in the third quarter of 2024, the shipments of the top five manufacturers have all achieved year-on-year growth, which is a reflection of this trend."

He added: "The new product launches of major brands this year have received positive responses, and leading manufacturers have achieved a better balance between hardware and software. This season's hardware highlights - including foldable models, ultra-thin designs, bold colors, and secondary screen designs on the back - have successfully attracted consumers' attention. Compared with previous quarters, many manufacturers have raised their production targets because the initial demand for new products exceeded expectations."

At the same time, Chinese brands have further expanded their global influence and gained more market share in the mobile phone market. Liu Yixuan told the 21st Century Business Herald reporter: "From the data point of view, in the first half of 2025, the share of Chinese brands in the overseas market has exceeded 50%, and now it is 52%. This number was only 11% in 2013. We also expect that Chinese brands will continue to shake the status of some established manufacturers around the world, as well as the global competitive landscape."

Liu Yixuan pointed out that in the past 10 years, Chinese brands such as OPPO, vivo, Xiaomi, Huawei, Honor, etc. have systematically expanded into overseas markets. They have also gradually implemented local production, establishment of local teams and long-term investment in overseas markets, realizing the transformation and progress from going out to taking root.

Entering a new stage, Chinese brands’ strategies in overseas markets are also upgrading. "As the market gradually becomes more saturated, even due to rising costs and fierce competition, against the backdrop of shrinking profits, manufacturers are also transforming and upgrading more diversified business models. Including some monetization of AI services, equipment finance, after-sales extended warranties, new revenue from media services, etc., will increasingly become the focus of manufacturers' follow-up strategies," Liu Yixuan said.

Overall, the recovery of the global market is not a simple recovery in volume, but also a structural restructuring. High-end, intelligent, and diversified revenue models are becoming new growth points for the global mobile phone industry. For Chinese manufacturers, how to achieve higher profits through ecological extension while maintaining overseas growth momentum will become a key proposition in determining the future global competition landscape.

China's market is reshaped and the top five are vying for hegemony in AI

Compared with the moderate growth of the global market, China's smartphone market is still in an adjustment cycle in the third quarter of 2025. Omdia data shows that the smartphone market in mainland China fell by 3% year-on-year in the third quarter, but the decline has narrowed compared with the previous quarter, showing that the market is gradually stabilizing.

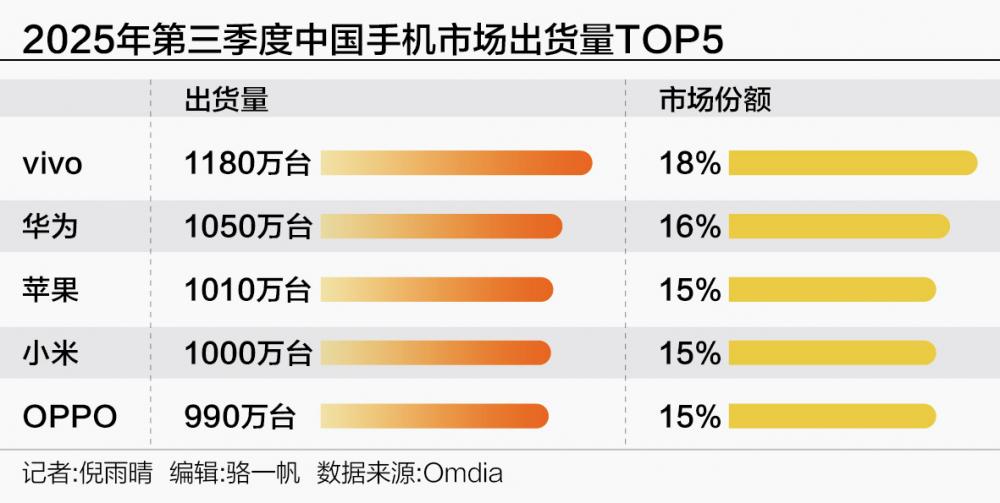

The gap between leading manufacturers has further narrowed, and competition continues to remain fierce. According to Omdia data, vivo returned to the first place in the third quarter with shipments of 11.8 million units, occupying 18% of the market share. Huawei ranked second, with shipments of 10.5 million units and a market share of 16%. Apple continued its gains from the previous quarter, shipping 10.1 million units, and its ranking rose two places compared to the same period last year, ranking among the top three in the market. Xiaomi shipped 10 million units and OPPO shipped 9.9 million units, ranking fourth and fifth respectively.

Omdia analyst Zhong Xiaolei pointed out: "Although the market has corrected for two consecutive quarters, the narrowing of the decline means that the periodic shipment fluctuations caused by the national subsidy plan at the beginning of the year are fading, and the market rhythm is gradually returning to normal. At the same time, the prudent shipment rhythm provides manufacturers with healthy inventory levels, leaving sufficient stocking foundation for the abundant flagship new product releases in the fourth quarter, the Double Eleven e-commerce peak season and the new round of subsidy policies."

However, Omdia chief analyst Hayden Hou said: "Despite the continuous correction, according to Omdia's forecast, mainland China's smartphone shipments are expected to achieve moderate growth in 2025 amid the background of national subsidies. Local brands are differentiating their products through appearance design, battery, camera capabilities, etc., and enhancing user experience through continuously upgraded AI functions and use cases to attract local users - Chinese users are the consumer group with the strongest propensity for AI in the world's developed markets."

Especially since this year, AI has become the focus of various manufacturers. At present, the development direction of AI mobile phones has moved from conceptual hype to system implementation. Manufacturers have begun to assume a key role in AI strategy in high-end product lines, especially domestic brands such as Huawei Honor, which are promoting AI from function to experience through continuous software optimization and ecological layout.

Liu Yixuan told reporters: "Although AI functions have not yet become the main driving factor for consumers to switch phones, more than 80% of consumers in the domestic market mentioned that AI functions are very important when considering their next mobile phone, and most people are increasingly concerned about the AI experience."

This also means that AI is becoming a potential standard feature in consumers’ purchase considerations. "Compared with when it first emerged, the depth of function embedding, user experience, and richness of application scenarios have all improved significantly in just one year. Especially in terms of high-end mobile phone product lines, it is also a particularly important product line for manufacturers to implement AI. We believe that on the AI track, if we can create more differentiated moats, we can change the market structure. Especially like Apple, the implementation of AI in the domestic market will be relatively slow." Liu Yixuan analyzed.

Overall, although the Chinese mobile phone market in the third quarter of 2025 is still undergoing adjustment, competition has shifted to "fighting for experience", "fighting for intelligence" and "fighting for high-end", and the top five camps are evenly matched. AI is becoming a new variable in the market structure. It has moved from a publicity stunt to a core capability and is changing the user selection logic. With the concentrated launch of new products in the fourth quarter and the arrival of the Double Eleven consumer season, China's smartphone market may usher in structural repair.