The latest report from Citrini Research, a market research organization, shows that by 2027, the LPDDR memory demand of NVIDIA's next-generation Rubin artificial intelligence platform on a single platform will exceed the combined usage of Apple and Samsung, the two major smartphone giants. This means that the competition for low-power DRAM in the server and AI fields will completely overwhelm the smartphone industry, and may even trigger chain reactions such as tight supply and rising prices.

The report points out that with the rise of new applications such as Agentic AI (AI with stronger autonomous decision-making capabilities), DRAM's core position in future AI servers will be further consolidated, and server platforms will continue to increase memory configurations to meet the ever-expanding model scale. Among them, the LPDDR capacity required for new-generation platforms represented by NVIDIA Rubin and AI-oriented products such as AMD MI400 has been described as "extremely amazing."

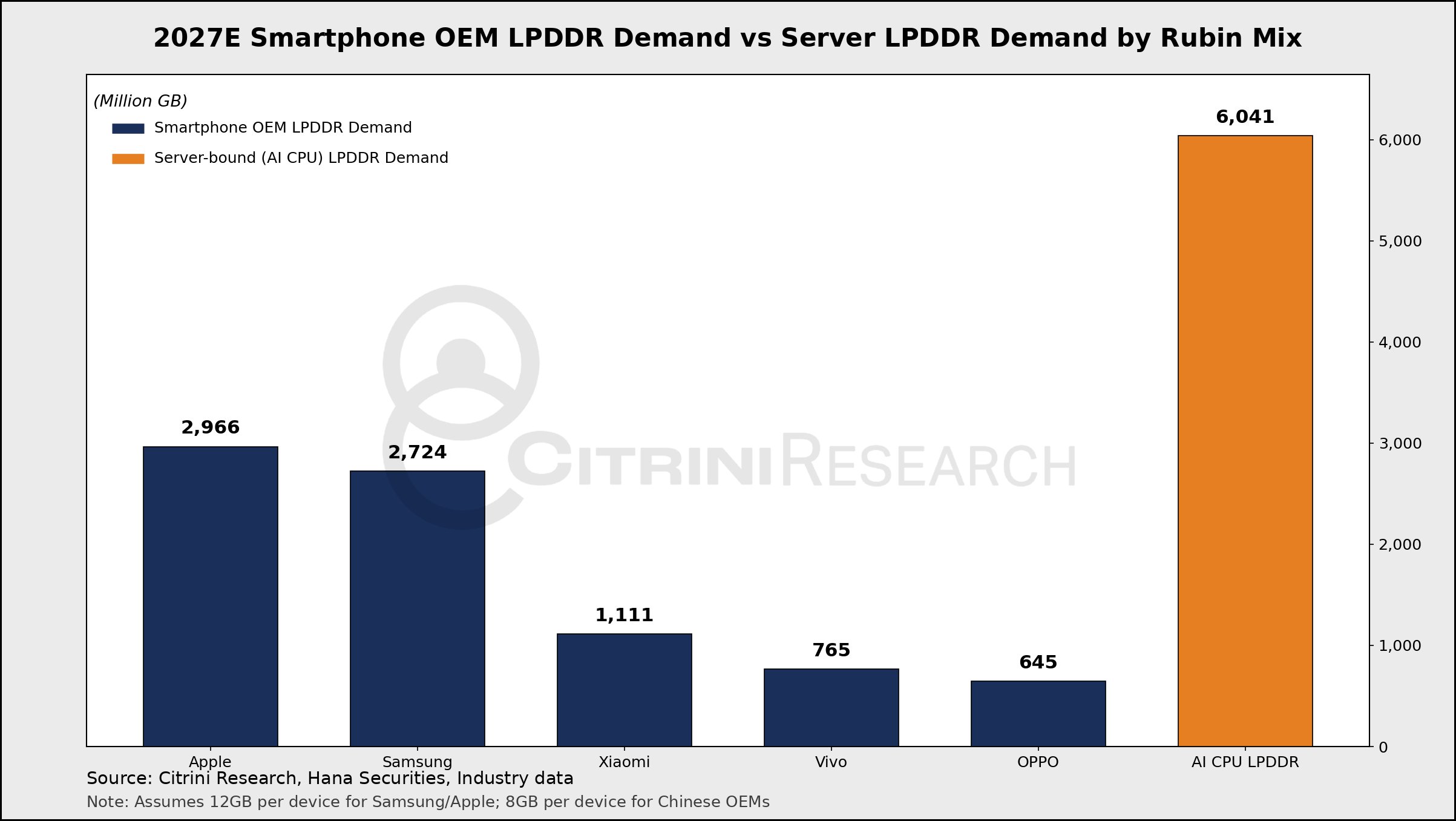

Citrini Research predicts that Nvidia’s Rubin AI platform is expected to consume more than 60 million GB of LPDDR memory in 2027. In contrast, in the smartphone camp, Apple is believed to remain the largest purchaser of LPDDR that year, with its iPhone series expected to consume approximately 29.66 million GB of LPDDR DRAM, followed by Samsung with demand of approximately 27.24 million GB. This means that Apple and Samsung’s combined LPDDR demand of approximately 57.2 million GB is still slightly lower than the consumption of Rubin Platform alone, which is approximately 6% higher.

From a technical perspective, LPDDR has become the "standard configuration" of AI servers because of its high capacity, compact packaging and relatively low power consumption, making it suitable for large-scale deployment in high-density racks and modular systems. The current industry focus is on the LPDDR5 and LPDDR5X standards, and many storage manufacturers are accelerating the launch of large-capacity solutions for the new generation of AI server scenarios.

For example, Micron has launched LPDDR5X SOCAMM2 modules with capacities up to 256 GB, targeting high-performance AI and data center applications. SK Hynix is mass-producing 192 GB capacity LPDDR5X SOCAMM2 modules for the NVIDIA Vera Rubin platform, providing high-density, low-power memory support for Rubin and related AI architectures. These products collectively point to a trend: the single-node memory configuration of AI platforms is rising rapidly, far exceeding that of traditional servers and consumer terminal devices.

In the AMD camp, the Verano series CPUs for AI and the MI455X accelerator card for Helios racks also support LPDDR5X memory, providing higher bandwidth and energy efficiency ratio for their AI workloads. Similar to Nvidia, the rise of these platforms has further pushed up the overall demand for LPDDR and increased supply pressure on the entire DRAM industry chain. The report pointed out that major manufacturers such as Samsung, SK Hynix and Micron have "betted fully" on the latest LPDDR technology and continue to expand production to cope with the next round of explosive growth in the AI ecosystem.

However, judging from the current production capacity and construction pace, it is difficult for existing factories to fully meet the explosive demand in the next few years, and new production lines and new facilities are still in progress. The time difference between supply-side expansion and demand-side explosion means that for a period of time, LPDDR supply is likely to remain tight, and competition between AI platforms and mobile phone manufacturers will become increasingly fierce. Especially in the high-end LPDDR5X segment, there is an obvious conflict between the configuration requirements of AI servers and flagship smartphones.

For the smartphone industry, the huge throughput of LPDDR by AI servers may have multiple impacts, including limited product supply, rising costs, and passive adjustments to memory configuration strategies for mid-to-high-end models. The report believes that similar supply and demand imbalances have already appeared in some technical fields, such as price fluctuations and shortages of some components, and may be further amplified in the LPDDR market in the future. As AI manufacturers accelerate the deployment of new generation platforms such as Rubin and MI400, smartphone manufacturers may have to make a more difficult balance between cost and configuration.

Overall, the "whale-like" demand for the LPDDR market from AI platforms such as Rubin is reshaping the structural focus of the DRAM industry, from smartphones as the main focus to rapidly shifting to AI servers and data centers as the core. In this new landscape, storage manufacturers strive for voice through production expansion and technology upgrades, while AI and mobile phone manufacturers compete for the same resource pool. The LPDDR supply situation and price trends in the next few years are likely to be dominated by the pace of expansion in the AI field.