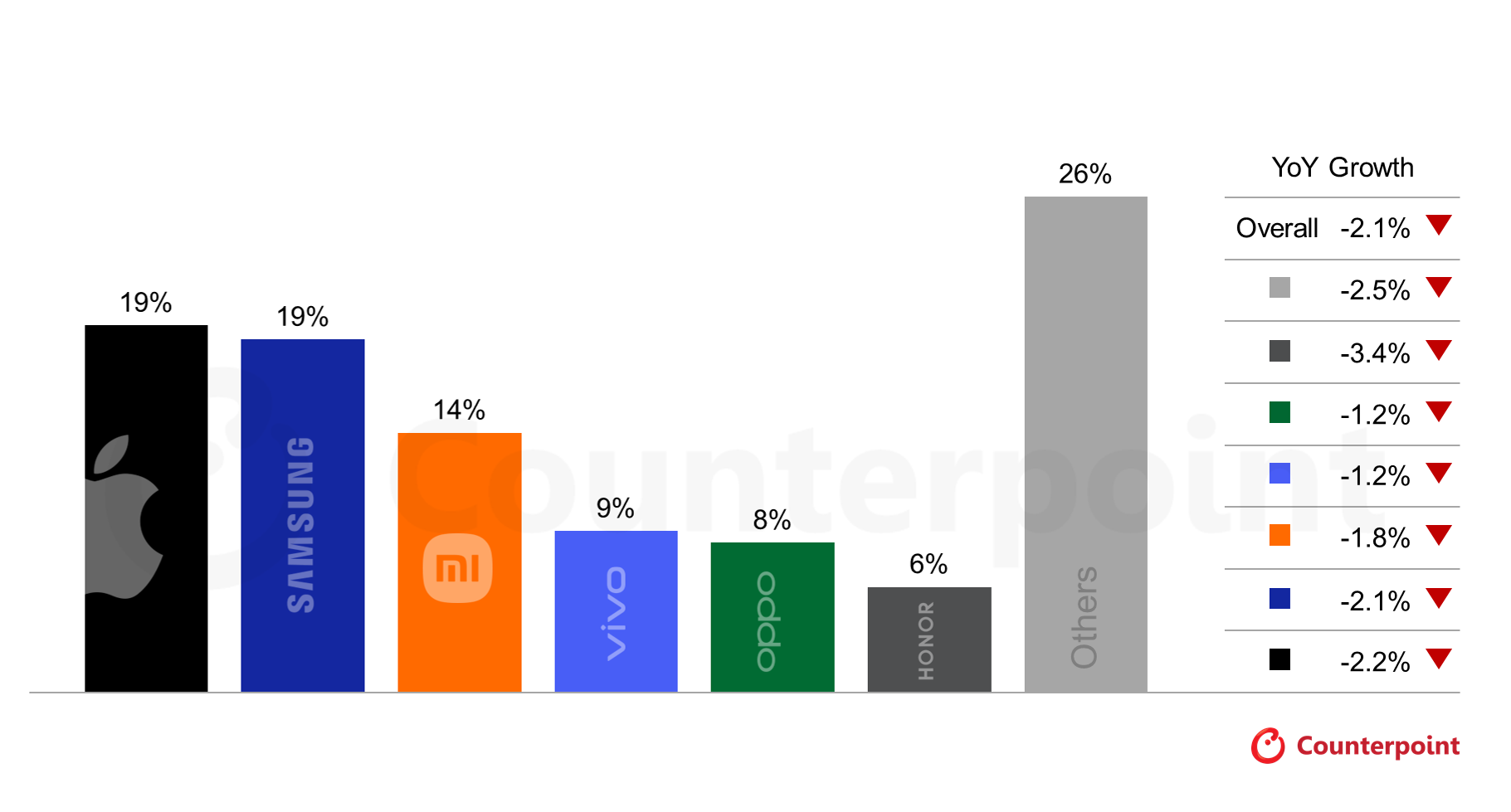

Market research firm Counterpoint recently lowered its forecast for the global smartphone market in 2026, predicting that shipments will decline by 2.1% year-on-year, instead of being roughly flat as previously expected. The core factor leading to this shift is the surge in memory prices in recent months, and it is expected that this round of price increase pressure will continue until at least the second quarter of 2026.

Counterpoint pointed out that memory chip prices will continue to rise sharply in the short term, and it is expected that by the second quarter of 2026, price levels may rise by up to about 40% on the current basis. Against this background, the bill of materials (BoM) cost of smartphones has increased across the board: the BoM cost of entry-level models has been approximately 25% higher than at the beginning of the year, while mid-range and high-end models have increased by approximately 15% and 10% respectively. If the price increase trend in the next quarter is realized, the overall material cost may increase by another 8% to 15% on this basis.

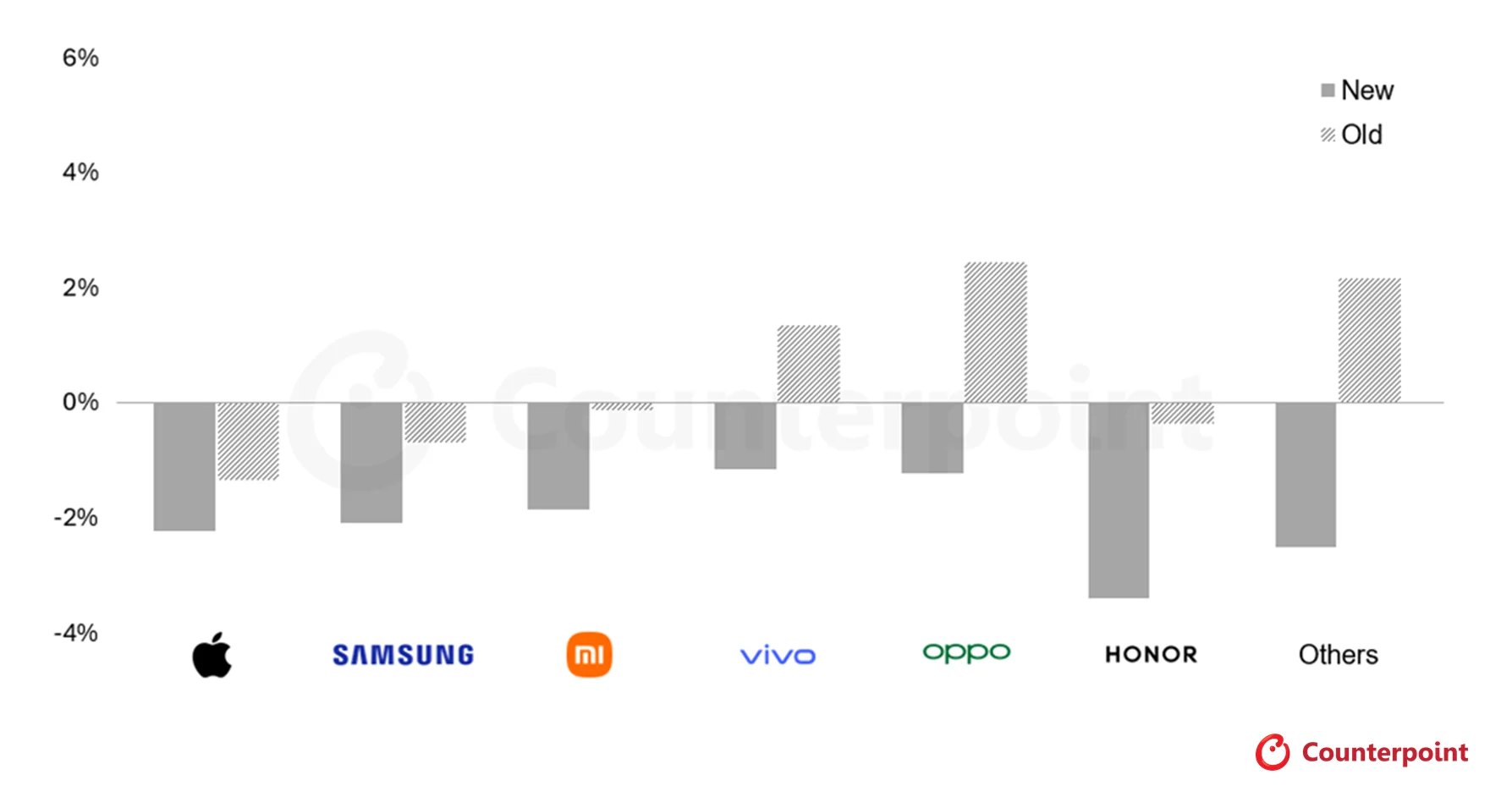

Under the dual squeeze of the demand side and cost side, Counterpoint predicts that the shipments of almost all major mobile phone brands will be affected to varying degrees in 2026. OPPO and vivo, which were previously expected to achieve shipment growth next year, have now been revised to decline; as for Xiaomi and Honor, which will be more affected in this round of adjustments, the decline in shipments is believed to be greater than previously expected.

In terms of large manufacturers, Apple and Samsung are also unlikely to be completely immune, but the overall degree of pressure is relatively light. Counterpoint senior analyst Yang Wang said that Apple and Samsung are "in a relatively more favorable position" in the next few quarters. They have greater room for adjustment between market share and profit margins, while manufacturers that lack such "buffer room" will face a more difficult balance test in the next year, especially many Chinese brands.

In order to hedge against cost pressure, smartphone manufacturers have begun to "increase revenue and reduce expenditure" by restructuring product lines and adjusting configurations. Counterpoint senior analyst Shenghao Bai revealed that on some models, manufacturers have already reduced key configurations such as camera modules and periscope telephoto solutions, display specifications, audio components and even memory capacity. In other words, consumers may see new models with more obvious configuration shrinkage in the same price range in the future.

At the price level, Counterpoint warned that the global average selling price (ASP) of smartphones in 2026 will be significantly higher than previous estimates. The agency originally expected ASP to grow by 3.9% year-on-year in 2026, but the latest forecast raised this figure to 6.9%. Since in mid-to-high-end and even flagship models, the memory cost accounts for a relatively small proportion of the total machine BoM, and the pressure is lower than that of entry-level and mid-range machines, analysts expect that manufacturers will more actively guide users to upgrade to high-end and high-priced models with higher profit margins to mitigate the impact of rising memory prices on overall profitability.