The latest memory industry research report released by TrendForce shows that driven by the continued surge in demand for AI and data centers,The imbalance between supply and demand in the global memory market has intensified. In the first quarter of 2026 (Q1), the prices of DRAM and NAND Flash products have increased significantly. The quarterly growth rate of many sub-categories has reached a record high, and the possibility of further upward revisions cannot be ruled out.

The research report pointed out that the core driving force for this price increase came from the explosive growth on the demand side.

As AI inference application scenarios continue to expand, major cloud service providers (CSPs) and server OEMs (Server OEMs) in North America and China have strong demand for high-performance memory. The shipment of complete PCs in the fourth quarter of 2025 exceeds expectations, further exacerbating the shortage of PC DRAM, and the inventory levels of leading PC OEM manufacturers continue to decline.

On the supply side, memory manufacturers are more optimistic about the profit prospects of the DRAM market and have shifted some production lines to DRAM production. As a result, the new NAND Flash production capacity has been compressed, and unit output can only be barely increased through process upgrades. Short-term production bottlenecks are difficult to alleviate. The bargaining power of original manufacturers has been significantly enhanced, and the market has obvious characteristics of a seller's market.

In terms of specific price increases, DRAM products have become the main driver of price increases.

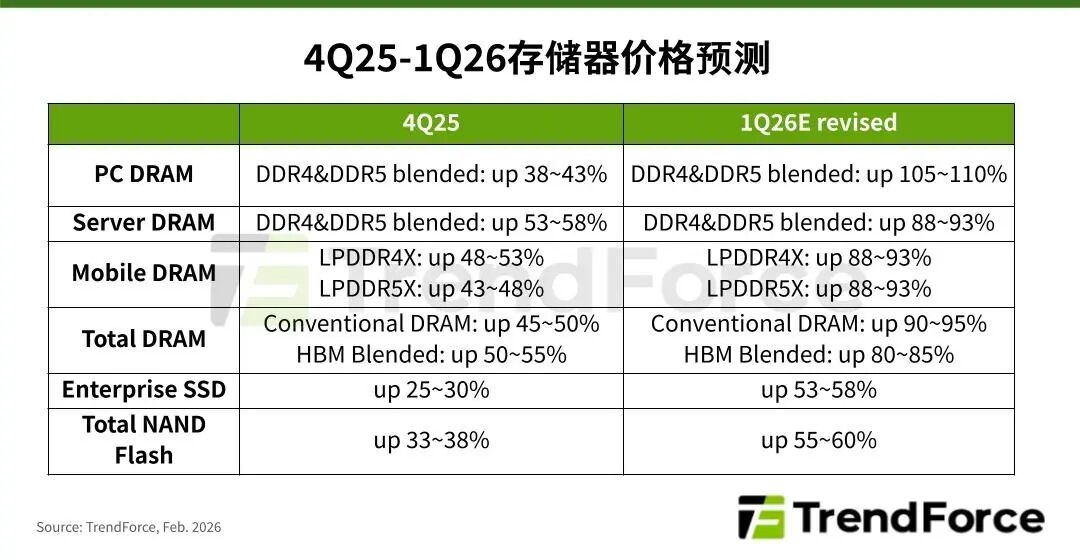

The overall Conventional DRAM contract price quarterly increase rate has been raised to 90%-95% from the 55%-60% estimated in early January;

PC DRAM (DDR4&DDR5 hybrid) prices are expected to increase by 105%-110% quarterly, more than doubling and hitting a record high;

Server DRAM prices increased by 88%-93% quarterly, and the contract prices of LPDDR4X and LPDDR5X in Mobile DRAM both increased by 88%-93% quarterly, both reaching the highest levels in history;

High-bandwidth memory (HBM) hybrid contract prices also achieved quarterly growth of 80%-85%.

NAND Flash products also experienced significant growth, with the overall contract price increasing quarterly from 33%-38% to 55%-60%.

It is worth noting that there are differences in the progress of memory purchase negotiations among mobile phone manufacturers.

The Mobile DRAM contract price for Q1 of 2026 for US mobile phone customers has been negotiated at the end of 2025. However, for Chinese mobile phone customers, due to the newly finalized contract price for the fourth quarter of 2025 and the long Lunar New Year holiday, relevant negotiations are not expected to make substantial progress until the end of February at the earliest.

This sharp increase in memory prices will have a significant impact on the production costs of terminal electronic equipment and supply chain stocking strategies.