A year ago, Xiaomi Motors just handed over its first complete quarterly financial report, and the capital market was excited. At that time, the monthly sales of the SU7 series were approaching 40,000 units, setting the record for the fastest delivery by a new force. Lei Jun wrote "Thank you all for your love" on Weibo, and everything is heading towards a standard Internet car-making myth.

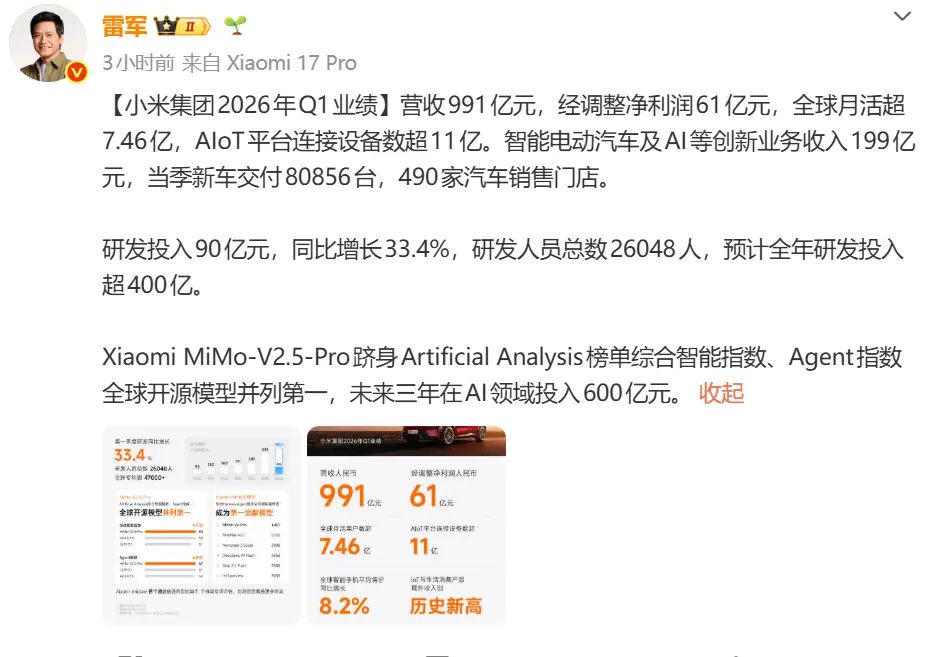

One year later, on May 26, Xiaomi’s 2026 Q1 financial report arrived as scheduled. Revenue from innovative businesses such as smart electric vehicles and AI reached 19.9 billion yuan, a year-on-year increase of 6.9%. 80,856 vehicles were delivered in the quarter, a year-on-year increase of 6.6%. At first glance, the numbers look okay.Revenue bucked the trend and rose slightly, while delivery remained stable. Against the backdrop of the group's total revenue falling 10.9% year-on-year and adjusted net profit plunging 43.1%, automobiles are almost the only segment of Xiaomi Group that is holding on. However, Xiaomi Motors, whose traffic is always online, has once again turned from profit to loss after experiencing profits for two consecutive quarters.

Lei Jun Weibo screenshot

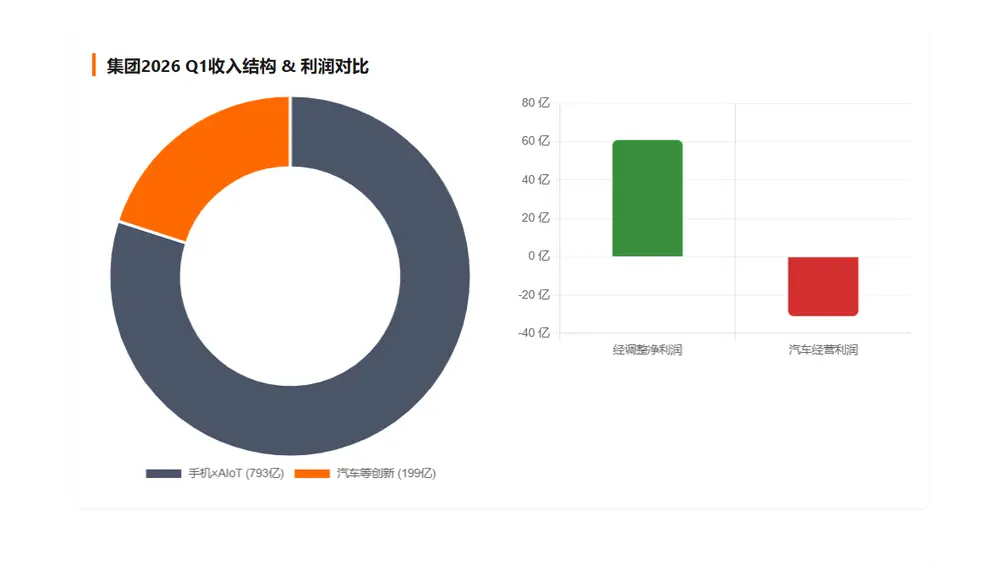

When the camera zooms out and the pixels decrease, the background of this picture begins to emerge. Among the 19.9 billion yuan in revenue from the automotive business, 19 billion yuan in revenue from smart electric vehicles, and only 900 million yuan from other related businesses. It is enough to see that the current story of Xiaomi Motors is "selling cars" from beginning to end, and the number of cars sold can be counted on one hand.

Looking at the global automobile market and looking through the history of the automobile industry, Xiaomi Motors is a very interesting sample. In two years, it has achieved the delivery volume of the first echelon of new forces with the smallest models in the industry. The two series SU7 and YU7 are phenomenal hits in any market around the world.

This is the first large-scale verification of "explosion logic" in the automotive industry, and it is a successful verification. However, this kind of thinking also brings many challenges to Xiaomi Motors today.

1

How long can the hit item last?

Looking through the Q1 financial report, there is a statement about the automobile product line that is worth reading carefully: "With the first-generation Xiaomi SU7 series discontinued and delivery volume reduced, a total of 80,856 new cars were delivered, achieving a year-on-year growth of 6.6%."

In other words, the old SU7 has done its best, and the current delivery depends entirely on the YU7 series.

In fact, the account can be calculated like this: Xiaomi Motors delivered a total of 80,800 units in the first quarter. The new SU7 contributed very little in the entire first quarter. After deducting more than 7,000 units of the new SU7, the remaining more than 73,000 units were basically taken by the YU7 series.

Xiaomi Motors in the first quarter was essentially a one-man battle mode in which a veteran was the main force and a new recruit was practicing.

The latest data shows that as of April 30, YU7 has been on the market for 10 months, with cumulative deliveries reaching 232,000 units. At the same time, April entered its first full delivery month after the new generation SU7 started delivery on March 23, with monthly retail sales reaching 26,826 units, accounting for 73% of Xiaomi Motors’ total sales in April. From a cumulative perspective, 26,000 units of the new SU7 were delivered within 35 days of its launch, and as of May 2, the number of locked orders has exceeded 70,000 units.

Data sources: Passenger Car Association retail data, Xiaomi’s official delivery announcement, and Lei Jun’s public statement. Some months are estimates

The waxing and waning of the two cars can be clearly seen in the April data. YU7 retail sales of 9,876 units that month continued to decline by 27% from 13,558 units in March. The sales peaked at 37,000 units at the beginning of the year and have been declining for three consecutive months. The new SU7 took over strongly with 26,000 units, bringing Xiaomi Motors' total delivery in April to just over 30,000 units.

If Xiaomi is placed in the entire territory of new forces, the structural risks of a single product will be further amplified.

Looking at the market of new players at the same level, in the first quarter of 2026, Leapmoon topped the sales list among new players with 110,200 units, Ideal ranked second with 95,100 units, NIO delivered 83,500 units, and Xiaomi ranked fourth with 78,600 units. Behind Zero Run are more than five product lines such as C series and T series running at the same time; Ideal relies on L6/7/8/9 plus pure electric i6, and the same five series dominate the world; Weilai's main brand is superimposed on Ledo and Firefly, with a model matrix of more than six series.

What about Xiaomi? There are two series, SU7 and YU7. In terms of the average contribution efficiency of each model, Xiaomi is more than one position ahead of all competitors. However, based on this, in terms of the possibility of being "stuck by someone's neck", Xiaomi has also thrown away all opponents, in more than one position.

This is exactly the ultimate interpretation of the "explosion logic" mentioned by Xiaomi Vice President Li Xiao in actual combat. In January this year, Li Xiaoshuang made it clear in an interview: "We hope that as few models as possible can generate as much sales as possible. The launch of new models will be more conservative than other manufacturers. In recent years, one new series will be launched a year."

Using a hot product to break through the price band and crushing opponents with efficiency has been proven by Xiaomi countless times in the field of consumer electronics. However, the rules of the game for cars and mobile phones are completely different. The development cycle of a mobile phone is 12 months and the life cycle is 18 months. If it overturns, it can be quickly iterated. The research and development cycle of a car is at least 36 months, and the life cycle is more than five years. If it overturns, there will be no turning back within three years.

Another consequence of having fewer models is even more fatal: if the rhythm of any one model is disrupted, the entire business line will be dragged down.

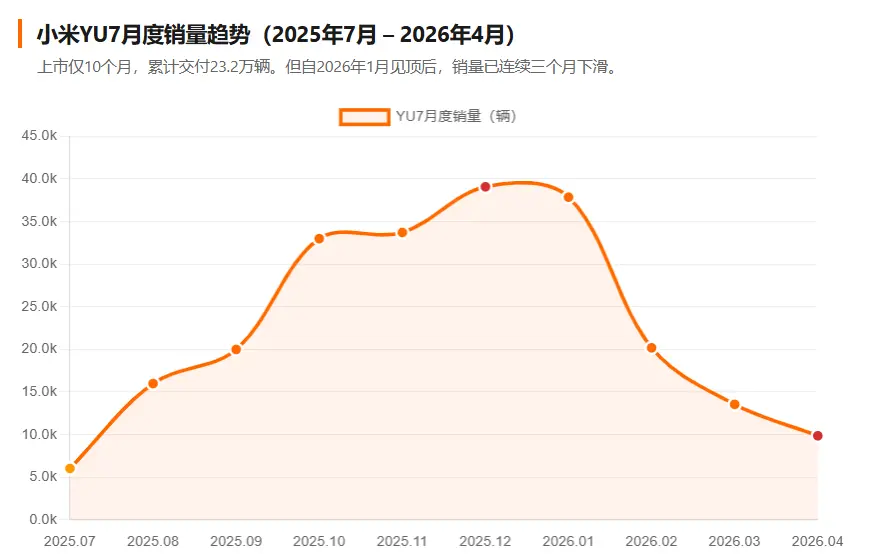

The sales trend of YU7 is the best example. Data shows that after YU7 delivered a peak of about 39,000 units in December 2025, it still maintained a high of 37,000 units in January 2026 and won the Chinese passenger car sales championship for the first time in that month. Then the situation took a turn for the worse, with only 20,196 YU7 units delivered in February, a sharp drop of 46.6% month-on-month; in March, it is estimated that about 10,000 units will be delivered, a drop of more than 60% from the peak. It took a quarter for a car to slide from nearly 40,000 monthly sales to 10,000 monthly sales.

When a car company's quarterly profit and loss can be simplified to an arithmetic problem of single model sales multiplied by single vehicle gross profit, what it exposes is not only a thin product line, but also a structural gamble that bets the fate of a billion-dollar industry on a product life cycle curve.

You must know that in the current fiercely competitive automobile industry, at the end of the long tail of popular products, there is no hedging, only a hard landing.

2

The dark side of gross profit margin being “kidnapped”

This "explosion hit" financial structure has left clear traces on the statements.

According to Xiaomi's financial report, the gross profit margin of innovative businesses such as smart electric vehicles and AI was 20.1%, a decrease of 2.6 percentage points from 22.7% in the previous quarter, and a decrease of 3.1 percentage points from 23.2% in the same period last year.

Data source: Corporate financial reports

In this regard, the official explanation is that it is affected by vehicle purchase tax subsidies, the decrease in SU7 Ultra delivery proportion, and the increase in the price of core components. To translate, fewer high-margin models were sold, and the proportion of low-margin models was passively increased. Coupled with the cost-end price increase, the overall gross profit fell accordingly.

So, why does the entire gross profit margin fluctuate when Xiaomi SU7 Ultra's delivery ratio drops?

In fact, the logic is very simple, and it is still because Xiaomi Auto has too few product lines. Among the new power car manufacturers at the same level, most car companies have more than three product lines. Therefore, a natural hedge can be formed between high-margin cars and low-margin cars, and the rhythm deviation of one car will not affect the overall situation.

However, when your revenue pool is basically supported by two cars, changes in the delivery rhythm of any one model will directly amplify into fluctuations in the gross profit margin of the entire business line.

Data source: Corporate financial reports

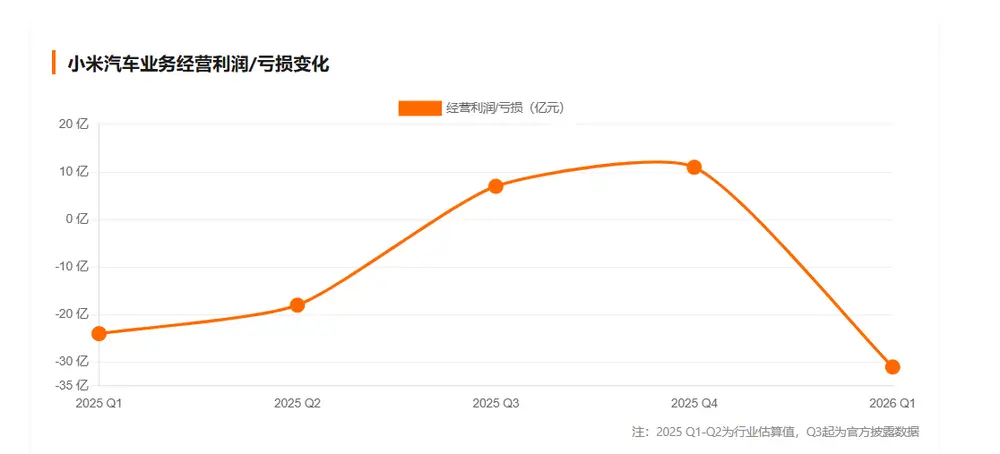

Even more troubling is the direction of the losses. In the first quarter of this year, Xiaomi's innovative businesses such as automobiles and AI suffered an operating loss of 3.1 billion yuan. You must know that only half a year ago last year, Xiaomi Motors had just achieved its first single-quarter profit in the third quarter of 2025, earning 700 million yuan; in the subsequent fourth quarter, operating income further expanded to 1.1 billion yuan.

After making profits for two consecutive quarters, the market has begun to use the framework of "new profit-making forces" to price Xiaomi Motors. Xiaomi Motors has once again turned a loss. The contrast between before and after is sharp. This kind of roller coaster profit curve is inevitable to a certain extent given the reliance on a single product line.

Because there are too few products and too little room for error, any external variable can easily penetrate the thin line of defense.

3

The market is waiting for Xiaomi to gather teamwork

The good news is that Xiaomi Motors obviously realizes that a single seedling cannot last long.

According to various information, Xiaomi has planned at least four new cars in 2026: YU7GT was released on May 21, with a starting price of 389,900 yuan, positioning it as the fastest SUV in New York history; the YU7 entry-level version starts at 233,500 yuan, with a weight loss of 115 kilograms ; The first extended-range SUV belongs to the new independent sub-brand "Xuntian", with the internal code name Kunlun N3. It is expected to be equipped with a large battery with a super 70-kWh battery and a pure electric range of 400 to 500 kilometers; there is also a suspected extended version of the SU7, with a length of nearly 5.1 meters, targeting the administrative market.

From pure electric to extended range, from entry level to performance, from five seats to seven seats, I have to say that Xiaomi’s product matrix drawing is beautifully drawn. If the four new cars ramp up as scheduled in the second half of the year, Xiaomi Motors will transform from "two series" to a real player covering multiple market segments.

However, "if" is also the two most expensive words in the capital market.

Among the above four cars, the YU7GT and YU7 entry-level versions have just been released, and the fastest ramp-up in production capacity will be in the middle and late Q2. The extended-range "Kunlun N3" and extended version of the SU7 are still in the "road test spy photos" and "trademark application" stages, and large-scale delivery is likely to wait until the end of the year or even 2027.

It can be seen that Xiaomi Motors will at least continue to use the "two single seedlings" model to carry on the entire first half of 2026. During this half year, Leapao is running five lines every month, Ideal is running five lines every month, and Weilai is running six lines every month. They are using matrix play to eat into every price band, while Xiaomi can only defend one area with one point.

Source: Xiaomi official website

In a live broadcast at the beginning of the year, Lei Jun disclosed the full-year delivery target for 2026: 550,000 vehicles. At that time, when faced with the doubts from the outside world that there were too few cars, he said: "For Xiaomi Motors, which has only entered the automobile market for two years, it is already very impressive to be able to sell 550,000 units."

This is true. The capital market does not look at success, but whether the delivery volume can support the PE multiple. The achievement of 80,000 vehicles in the first quarter was less than 15% of the annual target of 550,000 vehicles.

According to this goal, Xiaomi Motors needs to deliver more than 470,000 vehicles in the next three quarters, with a monthly average of more than 52,000 vehicles. If we really want to make Mr. Lei's dream come true, then the production capacity expansion, channel expansion and new car volume required behind this will be a tough battle.

It is worth mentioning that on the same day as the profit plummeting financial report was released, Xiaomi simultaneously announced a HK$20 billion share repurchase plan: In the next 12 months, the company can repurchase Class B ordinary shares in the market with a total value of no more than HK$20 billion.

The caliber of the company's announcement is to demonstrate confidence in future value, but if you think about it for a moment, you will understand that if a company's net profit fell, mobile phone shipments fell, and its automobile business turned from profit to loss in one quarter, and then spent 20 billion Hong Kong dollars to repurchase shares, is it telling the market "don't panic", or is it panicking first?

Reviewing Xiaomi's repurchase history in recent years: As of the announcement date, Xiaomi has repurchased approximately 399.6 million Class B shares for approximately HK$14.6 billion under the existing repurchase plan. Coupled with this new plan, the buyback intensity can be called radical.

In this regard, some market analysts said that the essence of this buyback is simple: when the market does not buy Xiaomi's growth story, Xiaomi will spend its own money to buy it. In Huxiu’s view, the core anchor supporting its “growth story” is precisely the future imagination of the automotive business.

Because a considerable part of the capital market's valuation of Xiaomi is based on the hope that Xiaomi Auto can quickly evolve from a "single product hit" player to a "multi-product matrix" player, thereby achieving sustained profitability under scale effects.

There is no doubt that there is a gap between a successful single product and a successful car company that requires multiple product cycles to fill.

When one quarter makes a profit of 1.1 billion, the next quarter loses 3.1 billion; when a car's gross profit margin fluctuates, it can directly determine the direction of the entire business line's gross profit margin; when a car's sales decline, everyone will begin to suspect that Xiaomi Motors' ceiling has been reached. This fragile balance is a structural flaw that cannot be covered up by any so-called "people, cars and family ecology" narrative.

The blueprint for product line expansion has been drawn up. If the four new cars can be collectively launched in the second half of the year, Xiaomi Motors will no longer be a "jungle player" fighting alone but will gather for the first time to "prepare for team battles."

But the premise of team battle is that your teammates must arrive on the battlefield on time. Among the four new cars, how many can be delivered on a large scale in the second half of the year, and whether the ramp-up speed can keep up with the patience of the capital market? If these questions remain unanswered, the valuation of Xiaomi Motors will hang on the extension of the single-product myth.

Once myths are questioned over time, they tend to have flaws. The progress bar of the annual target of 550,000 vehicles has just reached 15%, and the confidence of 20 billion repurchase still needs production capacity and delivery to realize it. Xiaomi Auto has more cards in its hands and the stakes are getting bigger. The next financial report cannot be the same story of two young people.