The latest forecast from research firm Counterpoint Research shows that with the demand for artificial intelligence hardware pushing up chip and memory costs, the global smartphone market will face contraction in 2026, and the industry as a whole will show a trend of "volume decreases and prices increase." Its latest report lowered its forecast for global smartphone shipments in 2026 by about 2.6%, with shipments expected to fall by about 2.1% year-on-year. It no longer expects only a few brands to decline, but "almost all major manufacturers" will record annual shipment declines.

The report pointed out that due to the rising demand for semiconductors and memory chips driven by AI development, the material costs of low-end smartphones have increased by 20% to 30% since the beginning of 2025, and storage prices are expected to continue to rise, and may rise by another 40% by the second quarter of 2026. Driven by this, the cost of the complete machine bill of materials (BOM) is expected to rise by about 8% to 15% more than the current high level, making it almost difficult for manufacturers to absorb the cost pressure on their own and will inevitably pass on part of the cost to end consumers.

Counterpoint predicts that the global average selling price of smartphones will increase by approximately 6.9% year-on-year in 2026. This will put greater pressure on price-sensitive entry-level and mid-to-low-end users, and may also prompt some consumers to extend the service life of high-end models and reduce the frequency of replacement while pursuing better experience and performance. However, overall sales are at risk of continuing to decline. The report specifically pointed out that low-end models will be the most severely affected market segment in this round of rising costs.

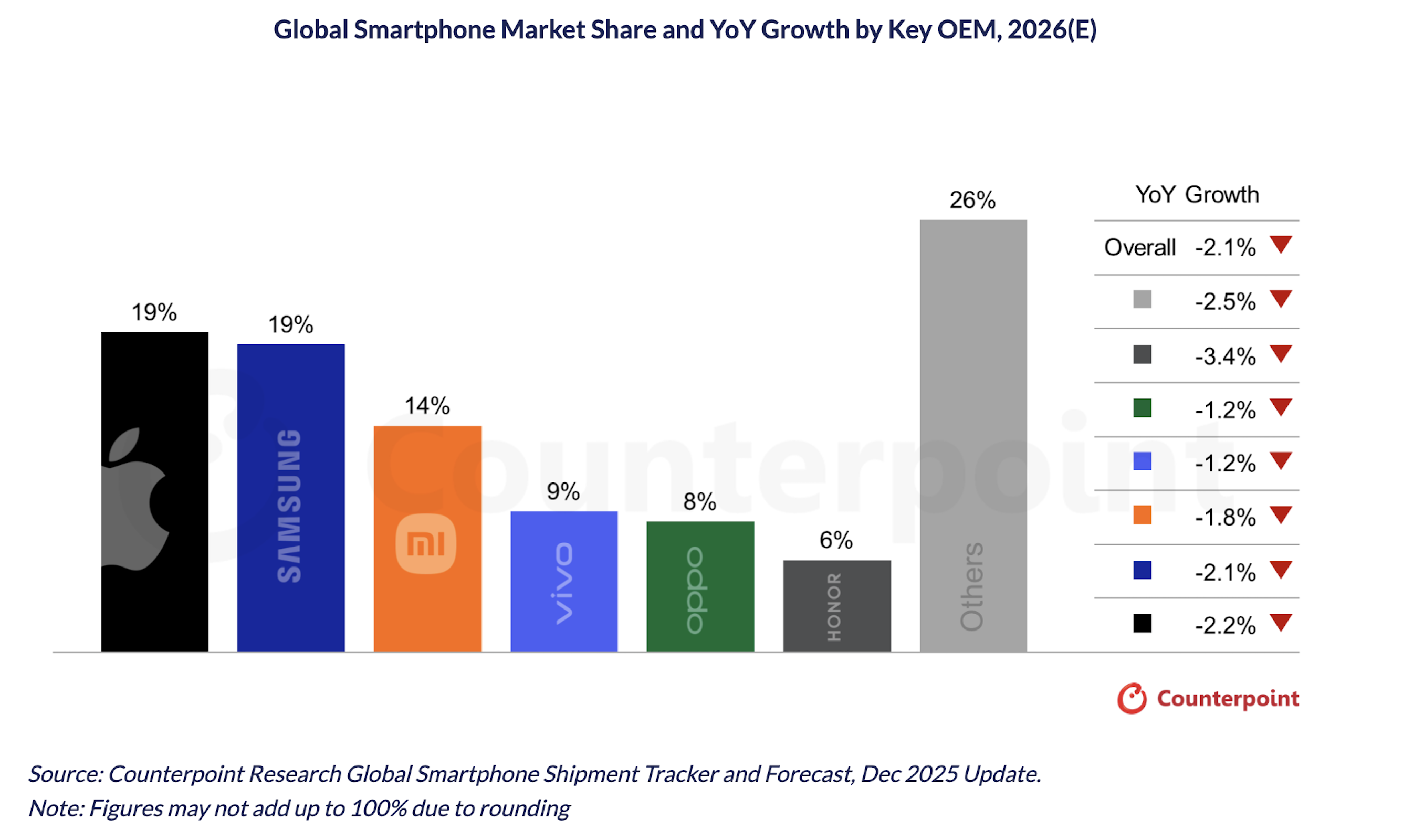

From a manufacturer level, all brands will be affected, but the degree of impact will not be the same. Thanks to their more robust financial conditions and relatively stable global supply chains, Apple and Samsung are considered to be more capable of withstanding stress, but the two companies' shipments in 2026 are still forecast to decline by about 2%. In contrast, Chinese manufacturers are under greater pressure as a whole, and their profit margins are further squeezed. The report stated that Honor's shipments may decline by more than 3%, and vivo and OPPO, which were previously expected to achieve growth in 2026, have now been revised to be expected to decline.

Among Chinese brands, manufacturers such as Xiaomi, Honor and OPPO have been named as facing a more severe market environment, and their strategic space is limited by the dual squeeze of declining profit margins and rising cost rigidity. As component prices rise and terminal demand weakens, how to control selling price increases without significantly damaging product competitiveness will become a key question that manufacturers must answer in the next year.

If Counterpoint’s revised forecast comes true, 2026 will likely become the second consecutive year of contraction for the global smartphone market. This not only reflects structural changes such as the maturation of the traditional mobile phone market and the extension of replacement cycles, but also demonstrates the power of the explosive expansion of the AI industry to reshape the entire electronic supply chain pattern - from data centers to smartphones, almost all terminals are paying for the same "track" of computing power and storage capacity.