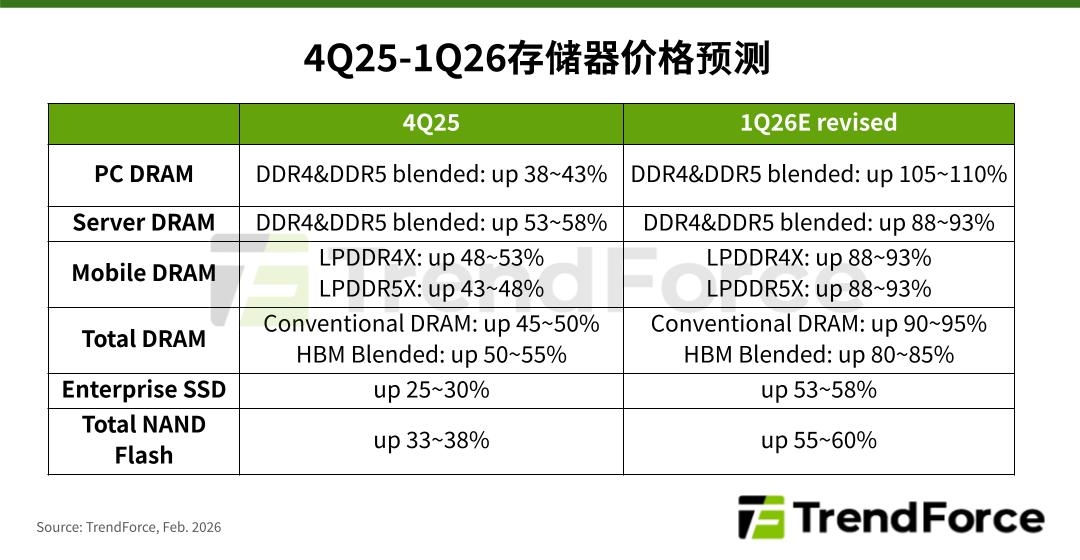

TrendForce's latest storage industry survey report shows that in the first quarter of 2026, the demand for AI and data centers will continue to exacerbate the global memory supply and demand imbalance, and the bargaining power of original manufacturers will continue to increase. Based on this, TrendForce has fully revised the quarterly growth rate of DRAM and NAND Flash product prices in the first quarter.It is estimated that the overall Conventional DRAM contract price will increase from the 55-60% quarterly increase announced in early January to 90-95%; the NAND Flash contract price will increase from the quarterly increase of 33-38% to 55-60%, and further upward revisions are not ruled out.

TrendForce points out that PC shipments in the fourth quarter of 2025 are better than expected, and PC DRAM is still generally out of stock. Even for tier-1 PC OEMs that are sure to obtain original supply, DRAM inventory levels are still declining.

With the seller's market pattern boosting contract price negotiations, the quarterly growth in PC DRAM prices in the first quarter of 2026 is expected to exceed 100%, reaching a record high.

In the server DRAM market, as buyers actively competed for original supply, server DRAM prices surged by approximately 90% in the first quarter, the highest level in history.

As for the mobile DRAM market, due to the ever-widening gap between supply and demand in the overall DRAM market, various terminal applications are competing to increase their quotations to obtain quotas.As a result, the contract prices of LPDDR4X and LPDDR5X in the first quarter were significantly increased to about 90% quarterly, which was also the highest in history.

Among them, the original factory's first-quarter contract prices for US mobile phone customers have been gradually negotiated since the end of last year; for Chinese mobile phone customers, the contract price for 4Q25 has just been finalized, and due to the impact of the long Lunar holiday, substantial progress will not be made until the end of February at the earliest.

In the NAND Flash market, the order volume in the first quarter significantly exceeded the production load of suppliers. However, the original manufacturers are more optimistic about the profit prospects of the DRAM market and actively convert some production lines to DRAM production, which further reduces the new production capacity of NAND Flash.

At present, the unit output can only be barely increased by upgrading the process, and the production capacity bottleneck will be difficult to alleviate in the short term.

In terms of commercial SSDs, as the supply gap continues to expand, buyers are aggressively hoarding goods to replenish inventory as soon as possible, pushing up the price of Enterprise SSDs in the first quarter of 2026, which will increase by 53-58% quarter-to-quarter, setting a record for the highest increase in a single quarter.