"Five days after the launch, Xiaomi Mi 17 series sales exceeded 1 million units, with the Pro Max version having the best sales. It has successfully established itself in the 6K+ price range and achieved a historic improvement in product structure." Lu Weibing, Vice President of Xiaomi Mobile, announced. However, the popularity of the high-profile first sale did not last. According to the observation data of technology digital blogger @RD, in the 41st week of 2025, the rankings of the three models of Xiaomi 17 series all dropped significantly: 17Pro fell to fifth place, 17ProMax fell to 14th place, and the standard version 17 dropped to 26th place.

Hot sales are temporary, but involution is continuous.

At present, China’s mobile phone market is still offline, accounting for about 60-70%. Also from an Internet brand, Honor's online and offline sales have changed from "37-open" to "73-open".

Compared with other leading manufacturers, Xiaomi's offline channel share still has a lot of room for improvement. In a market that is under internal control, Xiaomi must maintain growth and continue to attack the offline market. According to the plan, Xiaomi plans to hit 20,000 stores by the end of the year.

Here, mobile phone dealers have become outposts to help Xiaomi conquer the city, and their relationship with Xiaomi is one of love and death.

one

Fighting against the sinking market: young people are scarce and the fixed price is not effective

In its early days, Xiaomi relied heavily on online channels. Li Wanqiang, founder of Xiaomi, once revealed that “online accounts for about 70%, and nearly 30% of mobile phones are shipped through telecom operators.”

However, relying on online channels has caused Xiaomi mobile phones to encounter "dark moments". IDC data shows that Xiaomi’s full-year mobile phone shipments fell by 36% year-on-year in 2016.

In order to make up for its offline shortcomings, Xiaomi accelerated the expansion of offline channels in 2018. Xiaomi's financial report shows that as of the end of 2018, Xiaomi had established a total of 1,378 authorized stores, compared with only 62 a year ago.

Many dealers have joined Xiaomi one after another because they are optimistic about Xiaomi's ecological chain.

Liu Ming, a Xiaomi dealer in Guizhou, told "Financial Stories" that he initially chose to open a Xiaomi authorized experience store: first, because Xiaomi has rich ecological products, and the "department model" can share fixed costs such as personnel and rent; second, compared with other brands, Huawei's "368 merchants + goods purchase" model requires a capital threshold of tens of millions, and OPPO and vivo have dense stores in sinking markets and serious price involution. Xiaomi seems to be a "relatively controllable" choice.

However, dealers gradually discovered that selling millet requires low investment and low profits.

"The profits Xiaomi leaves for dealers are too thin." Zhang Lei, a former Xiaomi dealer in Jiangsu, said bluntly.

Zhang Lei revealed that the gross profit margin left by Xiaomi mobile phones to dealers is usually 10% to 12%. Although the gross profit margin is in line with the average level of the Android camp, the gap in "single machine profit" is obvious.

"Can the profit obtained from selling a Xiaomi mobile phone costing one to two thousand yuan be the same as selling a Huawei mobile phone costing five to six thousand yuan?" Zhang Lei asked rhetorically.

The dilemma of meager profits is not unique to the mobile phone business, but extends to the entire ecological chain of products. According to Zhang Lei's recollection, at a certain dealer meeting, a colleague once asked on the spot: "Your Xiaomi data cable sells for 17 or 18 yuan, why do we get less than 1 yuan?"

Faced with the problem of low profits, Xiaomi once instilled the concept of ROI (return on investment) into dealers and relied on high turnover to increase dealers' comprehensive gross profits.

In April 2021, Gao Ziguang, the former vice president of Xiaomi Group, said that at that time, most retailers could achieve a guaranteed annual investment return of more than 20% or 30%.

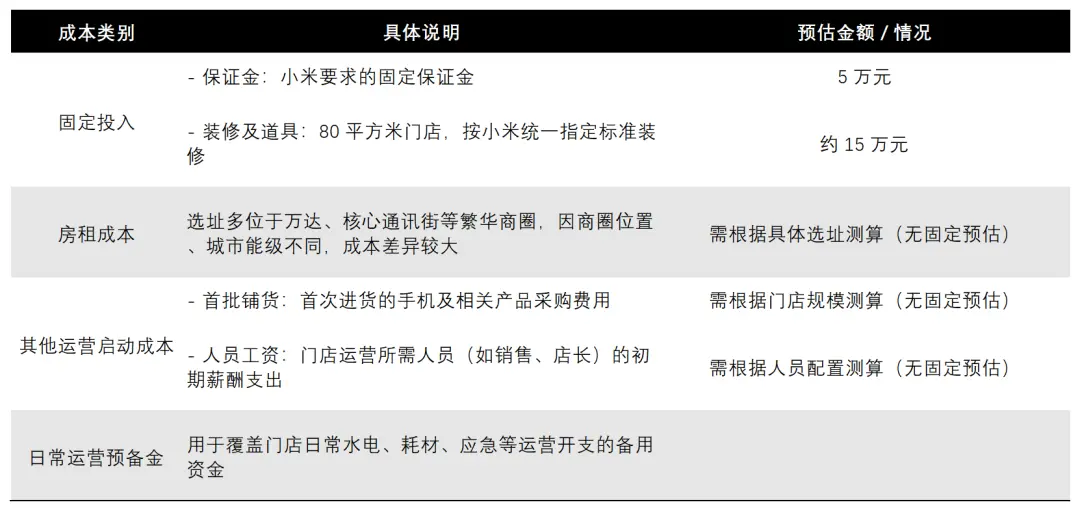

According to Zhang Lei's calculations, the initial cost of opening a Xiaomi Home store in a high-tier city like Suzhou is about 1 million to 1.2 million yuan, while in the central and western county markets it is 700,000 to 800,000 yuan.

Source: Provided by interviewee

Liu Ming, a Xiaomi dealer who opened a store in a county in Guizhou, encountered the problem of "too few young people."

"The main customer group of Xiaomi mobile phones is young people, but most of our young people go to the Yangtze River Delta and Pearl River Delta to work, and those who stay are mostly middle-aged and elderly people - there are not that many target customers."

Liu Ming's plight is not an isolated case.

Counties in the Midwest are losing young people. "Lookout" magazine once pointed out in the article "Why County Towns Can't Retain People" that counties have difficulty retaining talents due to lack of attractiveness. Without talents, they cannot attract high-quality enterprises, and the lack of good enterprises further aggravates the loss of young people...

Even more sluggish than the county market is the township market. "Many towns in the central and western regions are dominated by middle-aged and elderly people, and mobile phones exceeding a thousand yuan are considered expensive," Liu Ming has done research. A colleague he knew opened a mobile phone store in a town in Guangxi, and the payback period was as long as 6 years.

Because of this, most Xiaomi stores are concentrated in core areas of counties. Even in Tianying Town, Fuyang, Anhui, which was selected as one of the "Top 100 Towns in the Country," it is difficult to find a Xiaomi store."

The lack of target users and the long return cycle in the rural market have discouraged the majority of dealers. This may be the key reason why Xiaomi's "sinking into the rural market" strategy proposed in 2022 has failed to achieve large-scale breakthroughs so far.

The already scarce young customer base in the lower market has further reduced the conversion rate due to Xiaomi’s “unified electronic price label strategy”.

Liu Ming revealed that consumers in county areas generally have the habit of bargaining, and Xiaomi requires that the prices in offline stores must be consistent with the prices on Xiaomi’s official website.

Shop assistants are often questioned, "You said this is the price?" "If it's not cheaper, I'll go elsewhere."

In addition, it is normal for consumers to compare prices online and offline after entering a store. However, Xiaomi can control prices in its own channels, but it cannot restrict subsidies from third-party platforms such as JD.com, Tmall, and Pinduoduo.

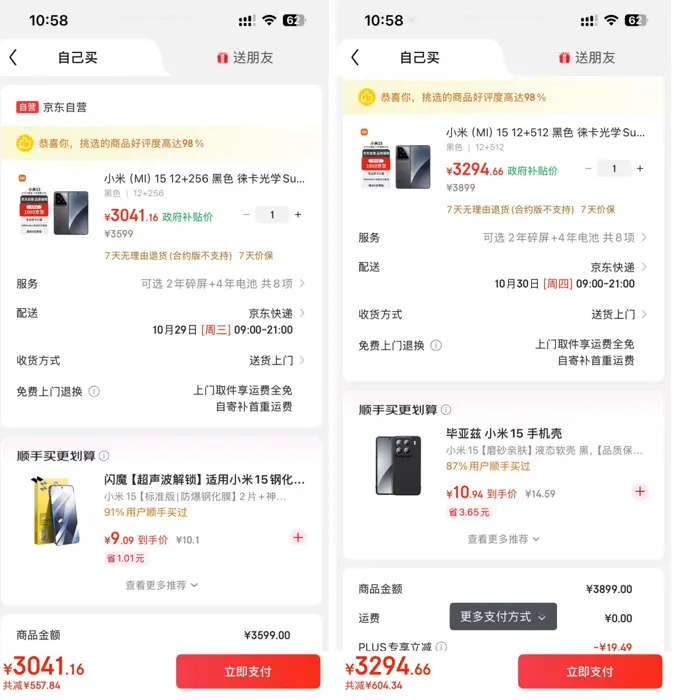

Take the 12+256GB and 12+512GB versions of Xiaomi Mi 15 as an example: the store prices are 3,599 yuan and 3,899 yuan respectively, while the prices after JD.com’s subsidies are only 3,041.16 yuan and 3,294.66 yuan.

Even if the store clerk emphasizes the store’s purchase gifts, trade-in, etc., many consumers still turn to online shopping. This causes offline stores to sometimes become “experience showrooms” and even leads to misunderstandings, “This boss is not serious in his business.”

OV, which has been deeply involved in the sinking market for many years, has flexibly positioned itself and understood the consumption logic of county areas.

Wu Hao, the owner of a vivo store in Zhoukou, Henan, told "Financial Stories" that vivo is well aware of the "acquaintance society rules" of the sinking market and does not adopt unified price tags.

For example, if a mobile phone is priced at 2,399 yuan, and the consumer bargains for 300 to 400 yuan and then sells it, he or she will feel that he or she is "getting an advantage." When an acquaintance receives the product, the store clerk says, "You were introduced by a friend, so I will give you a direct discount of XX yuan. In the future, you can introduce more customers to me." This can also make consumers happy to pay.

This problem of "acclimatization" also appears in the county layout of Xiaomi's home appliance business.

Xu Wei, a dealer of a certain home appliance brand in Hubei Province, said that many major home appliance manufacturers will "raise the front-end price", which not only satisfies the bargaining habits of consumers in county areas, but also facilitates dealers to maintain customer relationships; at the same time, different models will be distinguished online and offline to avoid direct price comparisons by consumers.

two

"Huaweiization" of Xiaomi channels: encryption and cooperation

In recent years, Xiaomi has been following Huawei's example, carrying out channel reforms, encrypting stores, implementing joint venture strategies, and bundling its automotive business to raise the bar.

According to "Photon Planet", starting in 2019, Xiaomi followed Huawei's 368 merchant model and divided dealers into blue blood, gold medal, TOP and other levels.

For example, the Mi Home store level is higher than the authorized store level. The higher the level, the better the policies you get, at the cost of opening more stores.

A Xiaomi dealer revealed, "Originally, the rebate for a single machine was about 20 yuan/unit, but after opening ten stores, the rebate can reach 40 yuan/unit to 50 yuan/unit. The temptation is not small."

Customer grading has driven the growth of the number of Xiaomi Home stores in the short term. In October 2021, the number of Xiaomi Home stores exceeded 10,000, doubling from April.

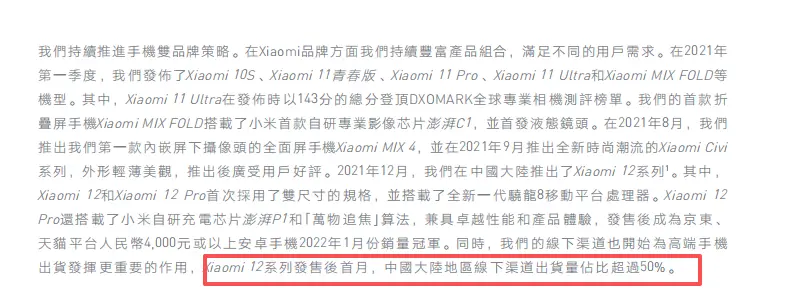

Xiaomi's sales structure has also changed simultaneously. According to Xiaomi's 2021 financial report, in the first month after the launch of the Xiaomi 12 series, offline channel shipments in mainland China accounted for more than 50%.

However, the lack of transparency in the design and implementation of customer rules has put both dealers under pressure. Lin Yang, a Xiaomi dealer from Henan, revealed that in name, blue-blood dealers "can earn an extra 1% commission by opening 10 stores", but in reality, the threshold of "monthly sales of 3,000 units" is implied.

Different from the distribution model of Huawei's 368 system, Xiaomi adopts the "Retail Pass Pre-deposit Model". The rights to the goods belong to Xiaomi, and the dealers are only responsible for "selling on behalf of".

The advantage of this model is that it does not require dealers to bear inventory risks, which reduces the pressure on dealers, but it requires extremely high turnover efficiency to maintain profitability.

"The rebates are limited. If the circulation speed of goods is not fast enough, it will be difficult to cover the operating costs," Lin Yang, a Xiaomi dealer in Henan, said frankly.

As Xiaomi's home appliances and mobile phone businesses gradually mature, coupled with the hot sales of Xiaomi's new energy vehicles after their launch in 2024, Xiaomi's offline expansion has accelerated again.

Lu Weibing revealed at Xiaomi's 2024 Q3 financial report meeting that Xiaomi has close to 14,000 offline retail stores and strives to reach 15,000 by the end of 2024 and 20,000 by the end of 2025.

In order to achieve the goal, Xiaomi guides some dealers to open 6-10 new stores, and dealers usually find it difficult to refuse. "If I don't open new stores, I'm afraid that big merchants will be introduced to the same business district - they will have high rebates and many resources, which will make it difficult to do business."

Due to its aggressive expansion, a large number of Xiaomi Home stores have emerged in core business districts across the country. However, because Xiaomi Home is mostly located in core business districts such as Wanda and Communication Street, forced store expansion has resulted in overcrowding of stores.

According to Cao Yang's observation, in Jieshou City, Anhui Province, Jianjian Road is a communication street and is home to three Xiaomi stores, two of which operate directly across from each other and the other is less than 800 meters away. Next door, Guangming Road in Linquan County is also a local communications street, and there are 4 Xiaomi Home stores within 2 kilometers.

However, Xiaomi's customer base in county areas is already limited. In the first half of the year, the national mobile phone subsidy overdrafted consumption, and stores were "clustered". In the past two or three months, single store performance has been significantly diluted.

Xiaomi dealers analyzed the reasons why Xiaomi implemented the "joint business" model. First, some small businesses became channels for scalpers to stock up on goods in pursuit of profits, leading to frequent cross-selling of goods, which disrupted Xiaomi's price system.

Second, contracts between Xiaomi and small businesses are signed once a year, and the channel stability is poor. For example, once dealers find it difficult to make profits, they may withdraw at any time, leaving Xiaomi with channel gaps and operational risks.

Third, Xiaomi's promotion of high-end strategy requires matching high-quality retail experience, brand image display, and stronger financial strength. However, small businesses often find it difficult to meet the corresponding standards.

Xiaomi’s new confidence in offline expansion comes from the hot sales of Xiaomi cars. The aforementioned 20,000 store target includes more than 200 Renchejia full-ecological integration stores.

Some dealers revealed that the application threshold for Xiaomi car stores is to open at least 15 Xiaomi stores first. Many dealers are willing to acquire more small business stores because of the overwhelming customer flow in their stores after the launch of Xiaomi's new cars and the fact that Xiaomi cars do not require dealers to bear inventory risks. "The threshold may become higher and higher in the future."

However, opening 15 stores means that dealers need to invest tens of millions of yuan. The high threshold has discouraged many Xiaomi dealers.

three

Dividends fade, dealers look to high-end and new national subsidies

In the first half of this year, many mobile phone stores had a good time relying on state subsidies.

After the national subsidies have gradually subsided, the business of mobile phone stores has become deserted. Liu Ming, the aforementioned Xiaomi dealer in Guizhou, revealed that the store's monthly shipments are now only a few dozen units. "It can't even cover the rent."

Zhang Lei, a Xiaomi dealer in Jiangsu, revealed that after his store was taken over by Dashang, the store's sales in July were only 4 to 50 million yuan, which was about 40% lower than when he was operating in April. "If it were not for the fluctuations in the national subsidy policy, it stands to reason that after Dashang took over, the performance would increase."

In fact, Xiaomi is not the only one. A dealer who has opened eight Huawei, Apple, and Honor mobile phone stores in Henan told "Financial Stories", "In the first half of the year, the state subsidies drove strong sales, and we did make money. However, the money earned in the first half of the year was almost lost in three months."

"The dividend period for mobile phone offline stores has long passed. Even if the stores are still profitable, I am very cautious about opening large stores or new stores," the above-mentioned Henan dealer revealed.

Amid the internal struggle, leading mobile phone manufacturers have adopted different strategies in order to attract and retain high-quality dealers.

With more than hundreds of thousands of stores, OV has penetrated deeply into the sinking market and accurately adapted to the bargaining habits and acquaintance society in counties. Although it is difficult for dealers to become rich, they can retain small businesses with "stable income".

Huawei stores invest a lot of money, and they are quite aggressive in stocking up, but relying on the brand premium to support it, the profits from a single machine are considerable. For example, Mate Master has been sold from 20,000 yuan to 60,000 to 70,000 yuan, which can attract large merchants with abundant funds.

Apple continues to consolidate its dealer ecosystem by relying on "full-link profits". Apple's second-hand mobile phone profits are also considerable, and the profit of second-hand mobile phones is often higher than that of new phones.

In contrast, Liu Ming was a little envious, "Xiaomi's profit margins are still relatively thin regardless of whether it is a new phone or a second-hand phone."

For example, Huawei’s Mate

Of course, Liu Ming has no plans to open a Huawei store yet, "the initial investment is too high."

Liu Ming, who is still sticking to Xiaomi, expects Xiaomi mobile phones to make breakthroughs in high-end products. "Dealers of low-end phones drink soup, and dealers of high-end phones eat meat."

But now, Xiaomi’s mid- to low-end models account for 70% of Liu Ming’s store shipments. "On the one hand, consumers' brand awareness of Xiaomi is still solidly based on cost-effectiveness. The more ecological chain products are sold, the more this impression is strengthened; on the other hand, Xiaomi lacks high-profit anchor products."

According to Xiaomi's financial report, in the second quarter of this year, the ASP (average selling price of a single machine) of its mobile phones declined, from 1,103.5 yuan per unit in the second quarter of 2024, a decrease of 2.7% to 1,073.2 yuan.

For comparison, Androidkenya data revealed that in Q1 2025, the global ASPs of Samsung, vivo, and OPPO (including OnePlus) were US$326, US$207, and US$269 respectively, while Xiaomi was only US$155.

Jeff Fieldhack, research director of Counterpoint Research, revealed that Apple’s ASP has exceeded the $900 mark in 2025.

Although the Xiaomi 17 series of mobile phones has helped Xiaomi open up a new world in the price range of 6,000+. But whether this high-end effect can continue is still a question mark.

Faced with the current situation of involution, hand dealers who are at the end of the industrial chain and have limited voice do not have much room for maneuver. They can only pin their hopes on manufacturers and the country.